Reports

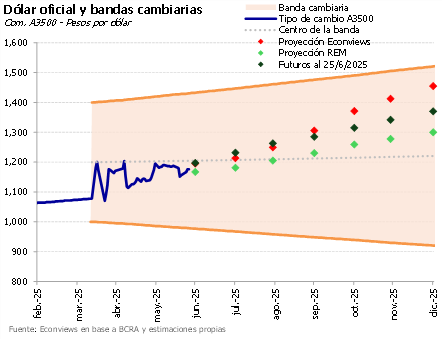

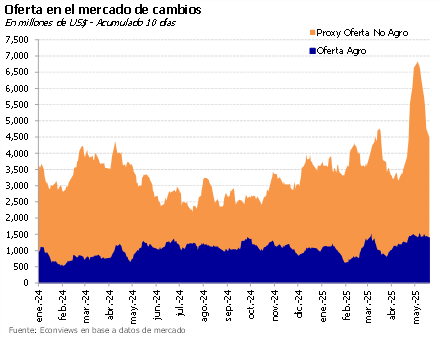

Un segundo semestre más picante. El gobierno termina el primer semestre con el dólar controlado cerca del centro de la banda. La segunda mitad del año luce un poco más desafiante. Los dólares del agro van a seguir fluyendo con fuerza hasta finales de julio, pero después esperamos que el tipo de cambio se acomode un poco más arriba. También habrá más demanda por turismo en los meses fuertes del verano europeo y por el ruido electoral. Se confirmó que el Banco Central intervino fuerte en el mercado de futuros en mayo, y no descartamos que siga haciéndolo.

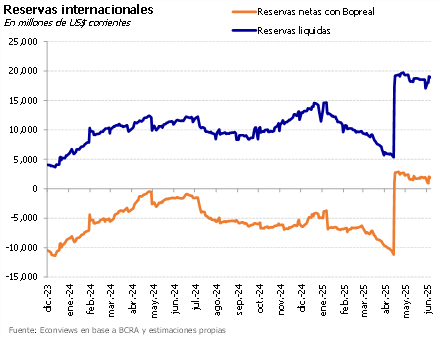

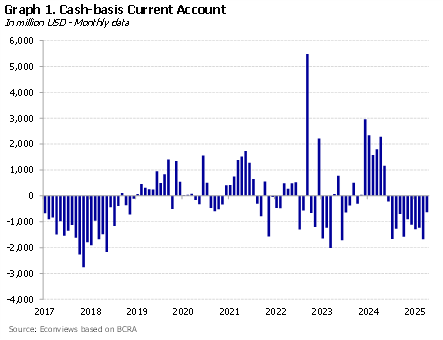

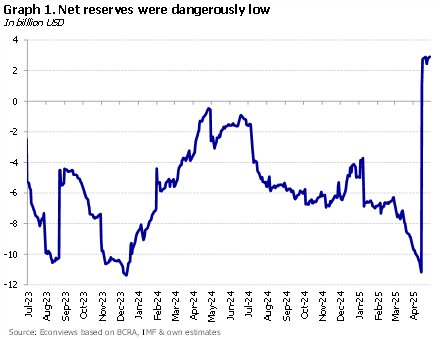

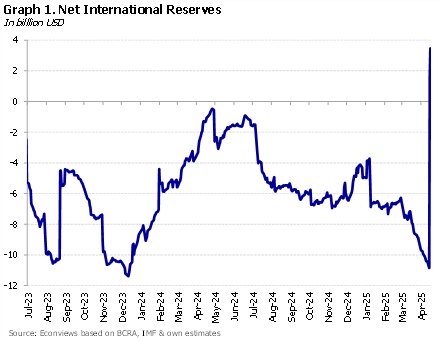

Seeking the waiver. The government has been “passing the hat” in recent days with new debt issuances. Bonte (hard peso) bonds have already contributed around USD 1.5 billion, to which USD 2 billion from the repo were added, bringing gross reserves above USD 40 billion and liquid reserves above USD 20 billion. To meet the IMF target, about USD 2.5 billion is still missing, but at least the government is showing a willingness to move closer, hoping to secure the waiver that would unlock the next USD 2 billion disbursement.

- weekly

The Evolution of the Economic Program: From Unconventional to More Orthodox

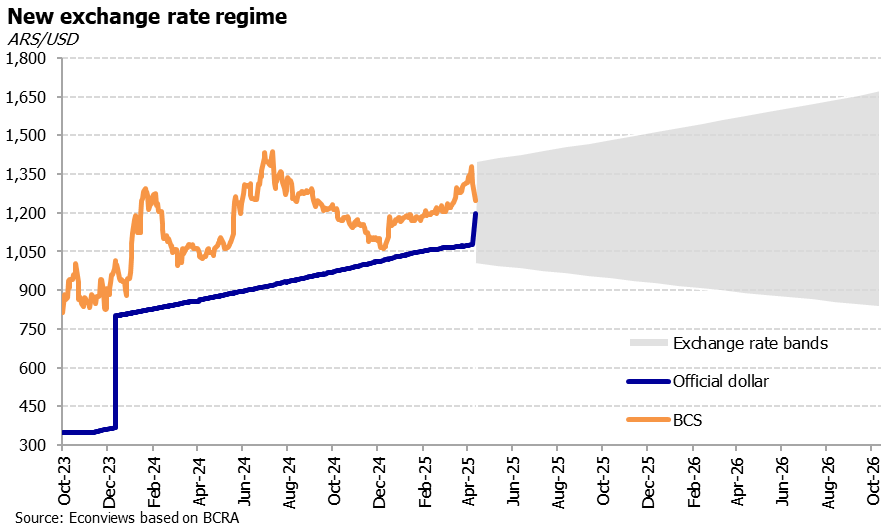

Monetary and exchange rate policy has been evolving since Milei took office. Initially, the program included several unconventional elements aimed at rapidly reducing inflation and providing an anchor for inflation. During that phase, interest rates were negative in real terms, the official exchange rate was quasi-fixed, capital controls remained in place, and there were multiple exchange rates. Over time, we transitioned to the current regime, where the anchor is money supply growth, real interest rates are positive, and the exchange rate floats within a band.

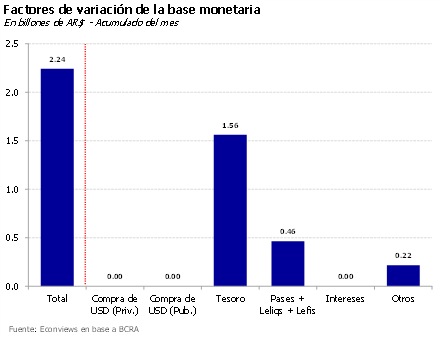

Anuncios importantes del BCRA. Esta semana, el Banco Central comunicó y/o formalizó una serie de cambios en la política monetaria, en coordinación con el Tesoro (para más detalles, ver la nota principal de este informe). En líneas generales, consideramos que los anuncios son positivos: apuntan a normalizar la política monetaria y facilitar la acumulación de reservas. Sin embargo, quedan algunas dudas sobre la implementación concreta de ciertos puntos.

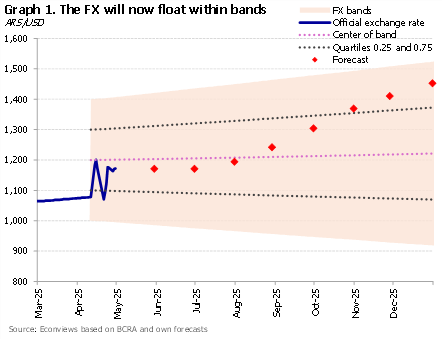

The debate on the exchange rate has calmed down now that the dollar floats within the band and its value is determined by the market. It’s true that it’s still not a clean float because there are many exchange controls in place for companies, but the spread with parallel dollar rates has disappeared and the Central Bank is not intervening. Now, the discussion has shifted to the level of international reserves — in other words, it’s moved from prices to quantities, although ultimately both reflect concerns about the sustainability of the external accounts.

Se develan los candidatos. Poco a poco se va configurando el mapa electoral de cara a las elecciones de septiembre y octubre. Esta semana, Cristina confirmó su candidatura como legisladora bonaerense por la tercera sección y reapareció en los medios. Será interesante monitorear cómo evoluciona la opinión pública con esta reaparición y si genera algún impacto en los activos argentinos. Según las últimas encuestas, la imagen de Milei volvió a repuntar, y, salvo la aparición de un cisne negro, esperamos que el Gobierno obtenga un buen resultado en las elecciones.

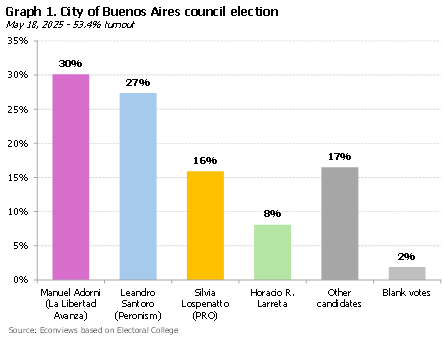

The political and economic climate has markedly improved since Argentina signed the new agreement with the IMF. On the political front, the government scored a key victory in the legislative elections of the City of Buenos Aires, which was a local election with strong implications at the national level. What would normally have been a minor election became a critical test of strength between Milei’s La Libertad Avanza (LLA) and Macri’s PRO. In the end, LLA secured nearly twice as many votes as PRO (30% vs. 16%), marking a major win for Milei and a serious setback for Macri, who lost a district that had been his stronghold in the last two decades.

Finally, the Treasury raised dollars by issuing a peso bond to international investors, who purchased it in dollars. Thus, the Treasury received fresh dollars, although the principal and interest payments will be paid in pesos. The move was a good one: it allowed the government to approach its reserve target with the IMF (which we all know it will not meet) and, at the same time, kept its promise not to purchase reserves within the exchange rate band.

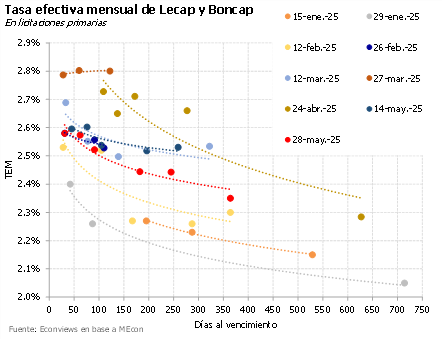

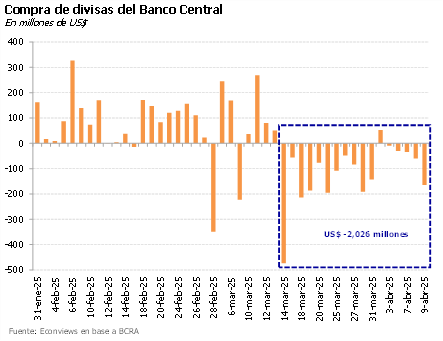

Leve suba del dólar. Después de algunas semanas bastante tranquilas, el tipo de cambio empezó a moverse un poco en los últimos días y ya acumula una suba del 2% desde el viernes pasado. El BCRA sigue sin intervenir dentro de la banda, pero sí metió mano en la curva de futuros, que parece ser la herramienta elegida para contener la presión. De hecho, el interés abierto subió a US$ 4,820 millones y las tasas implícitas siguen bastante por debajo de las Lecaps.

The government’s plan for getting Argentines to use their stashed dollars has finally been revealed, and everything indicates that the measures are less revolutionary than many expected. Even so, they represent an important step forward: by raising the minimum amounts for transactions that must be reported to the tax agency, people’s lives are simplified and the use of funds currently held in the informal economy is facilitated. This could translate into a slight increase in consumption and a greater circulation of dollars. However, if these bills do not enter into the financial system, they are unlikely to translate into more reserves.

Fuerte apoyo en las urnas. El domingo se celebraron elecciones municipales en CABA, donde el oficialismo logró un triunfo importante: desplazó al peronismo al segundo lugar y se impuso sobre el PRO en un distrito que los “amarillos” dominaron durante las últimas dos décadas. El resultado sugiere que el electorado respalda el rumbo del gobierno, valora la baja de la inflación y la estabilidad macroeconómica. Además, deja al oficialismo mejor posicionado para las negociaciones con el PRO en torno a las candidaturas en la provincia de Buenos Aires.

The deregulation and trade opening agenda continues at full speed. This is probably one of the areas where the government has made the most progress. Untangling the knot of regulations and opening the economy often involves confronting deeply entrenched business interests. However, the executive branch decided to take a further step on the eve of the elections in the City of Buenos Aires, which Milei’s party ended up winning.

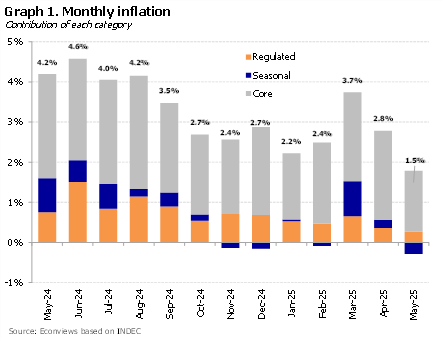

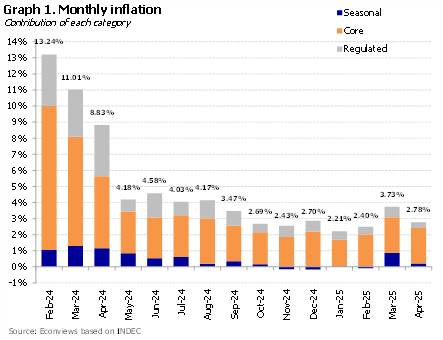

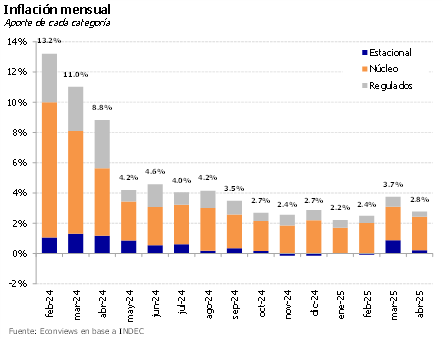

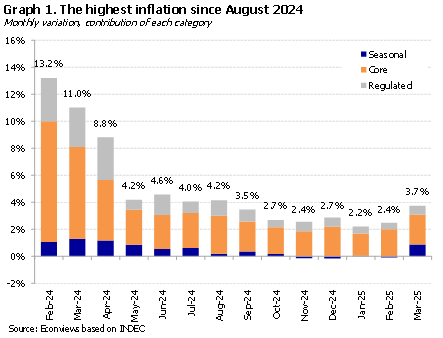

Objetivo logrado. Finalmente, el dato de inflación de abril fue muy bueno y vino en 2.8%, muy por debajo de lo que inicialmente se esperaba después del paso al nuevo esquema de bandas y muy inferior al 3.7% de marzo. El pass-through fue bajo, en parte porque algunos aumentos se adelantaron en marzo, y en parte porque el Gobierno fue muy hábil en contener las expectativas. La inflación núcleo se mantuvo estable en 3.2%, por lo que los componentes estacionales y regulados jugaron a favor. Nuestro relevamiento de precios de alimentos y bebidas anticipa una marcada desaceleración en mayo, y tampoco se espera demasiada presión desde los servicios, dado el estancamiento de los salarios, la baja en combustibles y la pausa en la recomposición de tarifas. Mayo apunta a ser otro mes favorable.

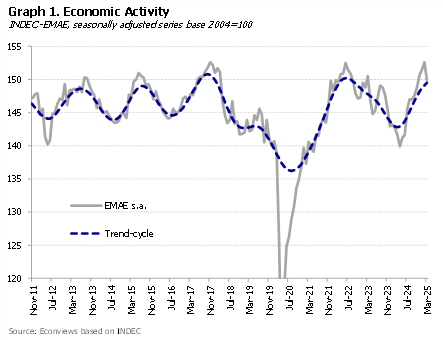

Following the new agreement with the IMF, the government announced the beginning of a new phase in its economic program — a turning point meant to mark the transition from stabilization to sustained growth. However, as the days went by, it became clear that this outlook was perhaps premature, and that we are actually heading toward a phase focused on consolidating stabilization. For now, the plan for sustained growth will have to wait. We’re still in the rebound stage after two consecutive years of GDP contraction.

Sigue la volatilidad. Después de unas semanas tranquilas donde el tipo de cambio osciló en torno a 1,180, ayer bajó fuertemente. Los futuros se movieron en la misma línea. No creemos que el dólar vaya al piso de la banda, aunque en los próximos meses deberían dominar los flujos de oferta de dólares por la cosecha y mantenerse tranquilo. Estimamos que en la zona cercana a 1,100 debería aparecer la demanda.

The negotiations with the IMF took longer than most people anticipated. Argentina wanted a USD 25 billion program while the IMF probably had in mind half of that amount. There were also discussions about the size of the upfront disbursement, as Argentina was requesting more dollars than the IMF was willing to provide. At the same time, the IMF was asking for more flexibility in the exchange rate regime, an issue that was raised in previous reviews, while Argentina wanted to avoid a step devaluation because it could put pressure on prices. One could summarize the discussions as more money in exchange for more flexibility in the exchange rate regime.

There is no second chance to make a good first impression. After implementing the new floating-withing-bands scheme, the government’s main objective was to avoid an overshooting of the exchange rate and, thereby, fuel the narrative that there was no step devaluation and that prices should not be adjusted.

The monetary policy outlined in the new program shows a shift toward a more conventional framework. Targets are now set for traditional monetary aggregates, such as the traditional monetary base or M2, instead of capping the broad monetary base — another Argentine invention that does not appear in any textbook. The rigid 1% monthly crawling peg, which was meant to perpetuate a concerning currency appreciation, was also abandoned. In its place, exchange rate bands were adopted, allowing FX to float between a floor of 1,000 and a ceiling of 1,400 pesos. But, as is typical in Argentina, the new regime brought several surprises, and in many cases, the main party caught off guard was the IMF.

Objetivo de pass-through cero. Tras el anuncio del nuevo esquema de bandas, el objetivo principal del Gobierno fue evitar un overshooting y minimizar el traslado a precios. Para presionar el tipo de cambio a la baja anunciaron la vuelta del carry trade para extranjeros (con 6 meses de permanencia, aunque pueden salir por CCL), dijeron que solo iban a comprar reservas en el piso de la banda, y presionaron al campo para que liquidara antes de que suban de nuevo las retenciones. También salieron con los tapones de punta contra empresas que mandaron listas con aumentos, arengando a no convalidar subas. Por ahora, el objetivo se viene cumpliendo: tras el salto inicial, el tipo de cambio retrocedió y muchas empresas dieron marcha atrás con los aumentos. En este contexto, esperamos que la inflación de abril se ubique más cerca del 3.7% registrado en marzo que del 5%, aunque hay arrastre de los últimos días de ese mes.

The first few days without capital controls were, without a doubt, a success for the government. The market reacted very positively to the announcements: far from testing the upper bound, the exchange rate settled closer to the lower band. The Merval index started off strong, later gave up some ground, but bonds remained firm and country risk dropped toward 700 basis points. The exchange rate spread collapsed.

Backed by a new USD 20 billion EFF agreement with the IMF, the Government has adopted a more flexible exchange rate regime, lifted several layers of FX controls, and introduced a more conventional monetary framework. We see these changes as very positive steps and a move toward greater economic rationality. Markets reacted clearly positively.

The government has announced the new exchange rate regime. At Econviews, we believe these measures are very positive, regardless of their potential short-term effects. The first stage of the stabilization plan had run its course, and a recalibration of the program was necessary.

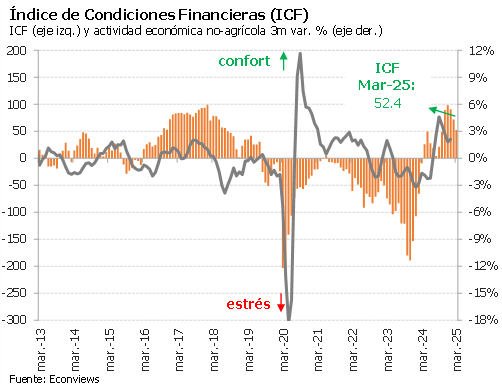

El ICF cayó 19 puntos en marzo y quedó en 52 unidades. Ya perdió 46 puntos en tres meses de 2025. Tanto las variables locales como internacionales empeoraron el mes pasado, con la incertidumbre por el acuerdo con el FMI y las políticas comerciales de Trump como problemas centrales. La medición no incluyó el crash financiero del 3 y 4 de abril, por lo que esperamos que el ICF mantenga la tendencia a la baja este mes.

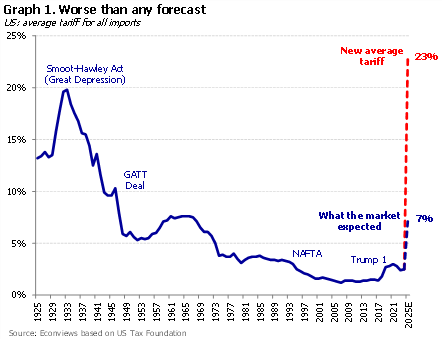

Volátil e impredecible. Ahora parece que la suba de aranceles se posterga por 90 días, lo que trajo algo de alivio a los mercados. Mientras tanto, las tarifas quedan en 10% para todos los países, excepto para China, que suben al 125%. En este baile, Argentina sigue el ritmo del mundo. El riesgo país, que venía aumentando en línea con otros emergentes de alto riesgo y había superado los 1,000 puntos cayó después de los anuncios de Trump. Las acciones argentinas también venían muy castigadas —en especial las energéticas, por la fuerte caída del precio del petróleo—, y recuperaron algo tras la postergación de los aranceles. Por primera vez, se ve a Trump retroceder en una postura que hasta ahora había sido tajante. De todos modos, da la sensación de que esta saga aún tiene muchos capítulos por delante, y China no parece dispuesta a ceder.

The future of exchange rate policy took center stage in the local economic discussion. Progress in negotiations for a new agreement with the IMF, combined with communication missteps by the economic team, raised doubts about the continuation of the crawling peg. This led to the longest reserves selling streak by the Central Bank during Milei’s administration and a rise in market exchange rates.

Another tough week for the government. As if dealing with Argentina wasn’t enough, the global context just got more complicated. The return of Trump went from being huge news to a major headache—not only because of the tariff policies, but also because expectations of a sharp recession triggered a global stock market drop, and the rise in country risk is pushing us further away from being able to rollover debt anytime soon. On top of that, uncertainty persists around the IMF program and the future of the dollar (or the poor peso), and the Senate’s rejection of Lijo and García Mansilla’s nominations to the Supreme Court marked yet another setback for Milei.

The government is losing momentum, and it now appears unlikely to have a smooth path to the October elections. After a first year in which everything went according to plan on the economic and political fronts, the outlook is gloomier due to some unforced errors and deteriorating financial conditions.

Algunas definiciones y otras incertidumbres. Sigue la saga del programa con el FMI en el que hay una clara pulseada. El gobierno lucha por conseguir la mayor cantidad de fondos sin moverse un centímetro de su política cambiaria, mientras el FMI quiere canjear plata por más flexibilidad. Un partido con final abierto y con dos escenarios claros; uno con el siga siga y otro con salto cambiario. Argentina ya habría conseguido unos US$ 8,000 millones al contado y el resto en cuotas, pero quiere más. Al FMI le gustaría una flotación y unificación del tipo de cambio, pero no se sabe si tiene la fuerza para imponerlo. La decisión final seguramente va a ser política y mucho dependerá de cuánto se juegue Trump para apoyar a Milei. Las partes tienen presión para llegar a un acuerdo rápido porque las reservas están cerca de un piso y los mercados nerviosos.

The government has found itself in a dilemma that now seems difficult to resolve. The strategy was diametrically different from Macri’s. Quick on fiscal matters, but with infinite patience to lift FX controls. However, the exchange rate problem never stopped being there, and managing expectations and timing to resolve it has become crucial.