The Promise of Buying Reserves Becomes a Reality

When it was announced in December that the Central Bank would begin accumulating reserves in 2026, many of us were skeptical. The government had consistently missed this explicit target within the IMF program throughout last year and had operated on the edge regarding the external front—to the point of needing a “Trump bailout” to avoid […]

First Steps of the Year: Progress, Tensions, and Pending Issues

A new year begins with many challenges but also with hope. Fortunately, it starts with an approved Budget Law and a good chance of moving forward with labor reform. Also, as expected, debt payments were made, providing some peace of mind. However, the challenges remain significant: taming an inflexible inflation rate, ensuring the recovery reaches […]

The Band Widens and the Anchor Loosens

The government has decided to shift the focus of its program. The exchange-rate band, which until now had been adjusting at a monthly pace of 1%, will now move in line with past inflation, closer to 2%. More importantly, it announced an explicit plan to accumulate reserves, with monthly purchases of around USD 800–1,000 million. […]

An Exchange-Rate Anchor Without Reserves

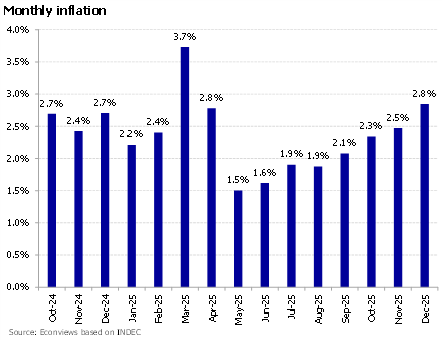

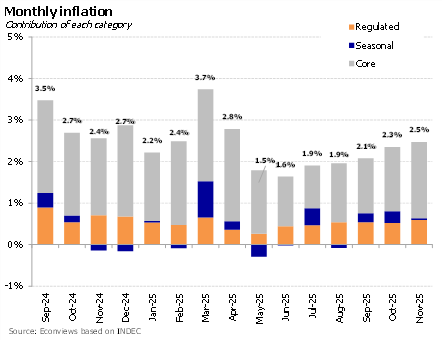

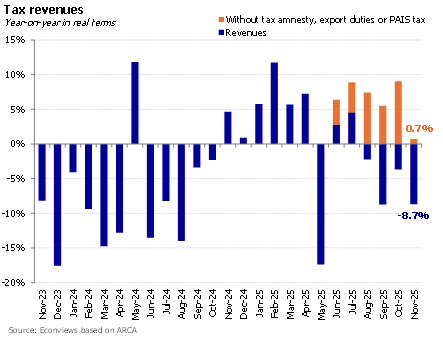

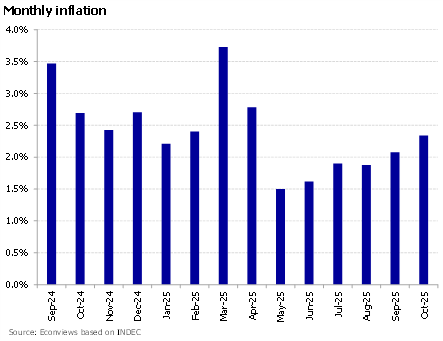

November’s inflation print came in broadly in line with expectations, but it still raised a yellow flag. It is not alarming for now, although the trend over the past six months has clearly been upward. Core inflation, which better captures underlying dynamics, rose to 2.6%, its highest level since April, and year-on-year inflation accelerated […]

Returning to the Markets

As we anticipated in our last editorial, the government announced with great fanfare that Argentina will once again place dollar-denominated debt. The January maturities accelerated the timeline, and “Toto” decided to step onto the field to seek financing in the local market.

In Search of Dollars for the January Payment

As the year-end toast approaches, the market is beginning to eye the January calendar with some concern. And with good reason: Argentina faces capital and interest maturities in foreign currency totaling around USD 4.2 billion, and the Treasury’s dollar coffers are empty. There is no time to buy dollars in the market, nor has the […]

Our View

Rates keep falling. Short-term interest rates (repos and caución) have stabilized around 20%, with the Central Bank lowering the floor to 20% in the simultáneas (reverse repo) operations market. This pulled the rest of the curve downward and improves the rate at which the Treasury will be able to roll over its debt in tomorrow’s […]

Trade Agreement: The Biggest Gain Is Institutional

The framework agreement on trade and investment with the United States was finally announced. It is not a free trade agreement nor a deep accord endorsed by the Congresses of both countries, but rather a government-to-government understanding aimed at boosting the bilateral relationship and strengthening U.S. influence in Argentina, which Washington views as a strategic […]

From Relief to the Challenge of Macroeconomic Consistency

Milei’s economic program seems to have entered a new phase. After the confidence shock triggered by the election victory, signs of a more normalized economy are starting to appear, with interest rates falling to more sustainable levels — both for public debt and for overall economic activity.

What Could Change in the Economic Program

The surprising and impressive victory of LLA in the elections completely reshaped the political and economic landscape. The ruling coalition exceeded its minimum goal (securing one-third of the Lower House) and, together with PRO, also achieved one-third of the Senate—leaving Peronism without a majority in that chamber for the first time since the return of […]