A Transparent but Unclear Central Bank

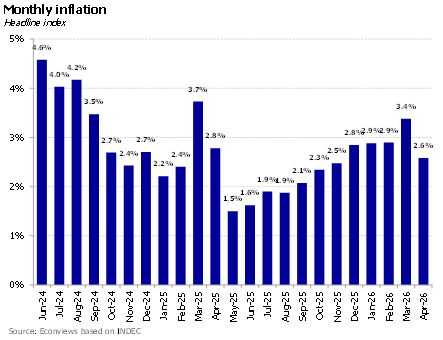

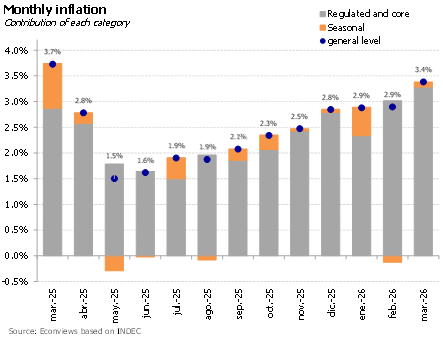

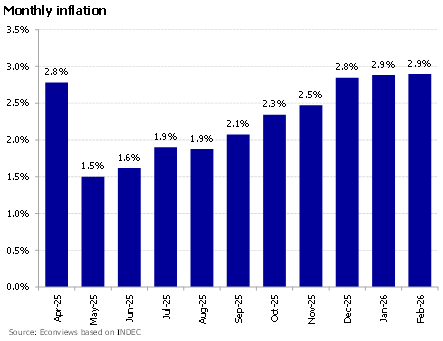

In April, inflation fell for the first time in 10 months. This is a positive figure considering it had been on the rise and reached 3.4% in March. There is no doubt that this figure was an isolated event because, beyond the ups and downs of recent months, inflation has maintained an average of around […]

Fitch Upgrades Argentina’s Rating — Will Argentina Take the Leap?

If we look at the regional country-risk rankings, Argentina is still the black sheep of Latin America. Despite the sharp improvement in sovereign spreads since Javier Milei took office — with country risk falling from nearly 2,000 basis points to around 515 today — Argentina remains near the bottom of the table, ahead only of […]

Our View: Country risk, Central Bank, and credit

Investors are watching Argentina cautiously. After two weeks under pressure, sovereign bonds turned green again and country risk dropped to around 550 basis points. The previous rise had gone against the trend in other emerging markets and came amid rumors of a possible operation with the World Bank and the IDB to guarantee bank loans. […]

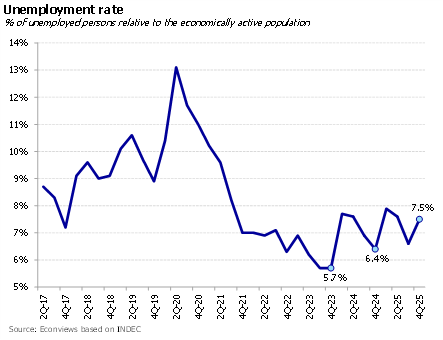

A Two-Speed Economy Doesn’t Work for Everyone

The data are becoming increasingly clear and are beginning to speak for themselves, pointing to a “two-speed” or bipolar economy. The problem for the government is that the sustainability of the program depends on growth reaching a broad share of the population. Instead, what we are seeing is that the winners so far are a […]

Is It Politics or the Economy?

Javier Milei’s economic program is going through a critical moment. Inflation has risen over the past 10 months, reaching a peak of 3.4% monthly in March. At the same time, there are clear signs of stagnation—or even contraction—in industrial production, construction, mass consumption, and employment. Wages have been consistently losing ground to inflation, resulting in […]

Green Shoots on the Horizon

After years of rollercoaster mode, the Argentine economy has entered a less dizzying phase. Weekly shocks and abrupt shifts in sentiment have subsided, which is, in itself, good news. Within this framework of greater stability, February and March will likely stand out as the weakest months of the year in terms of activity and inflation.

Our view: Echange Rate, Interest Rates and Debt

Strong purchases in the first quarter. In recent days, the Central Bank stepped on the accelerator and closed the first quarter with foreign exchange purchases exceeding USD 4.3 billion, at a pace of nearly USD 1.5 billion per month. With the start of the main harvest season, the Central Bank now has the opportunity to […]

Activity, Rates and Inflation

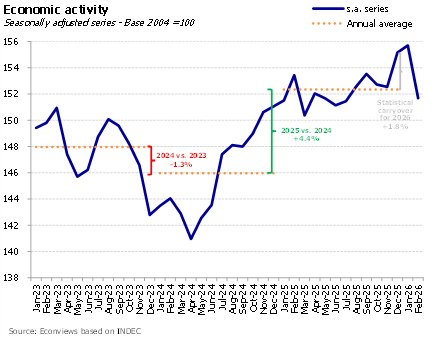

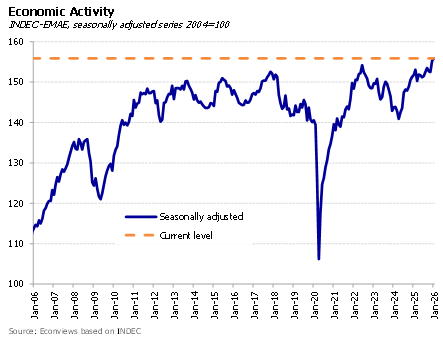

What the Data Says About Economic Activity. The debate over economic activity gained intensity following the publication of the 2025 Q4 GDP and the January EMAE (Monthly Estimator of Economic Activity), which showed that the aggregate economy is growing. In January, even lagging sectors such as industry and construction showed a monthly recovery. However, […]

Rate Relief, as Long as the Dollar Holds

It is still too early to draw conclusions, but there are signs that the Government is shifting its monetary policy stance. Despite several officials doubling down in recent weeks to argue that the economy is growing and that jobs are not being lost, this week’s data and the policy decisions themselves challenge that narrative. The […]

Between Inflation and the Aftermath of Argentina Week

Last week kicked off with high hopes around the Argentina Week in New York and ended on a sour note with the February inflation print. The timing for the event was far from ideal — the Government went out to sell the country to the world while investors had one eye glued to the Middle […]