We offer reports on the Argentine economic and financial situation, focused on key aspects such as the level of activity, fiscal accounts, inflation, interest rates and exchange rates.

Presentations

We make in-company presentations on the Argentine and international economic situation, adjusting to the client's needs.

Consultations

We are available for specific queries from our clients on current issues via phone or email.

Forecasting

We prepare detailed long-term economic forecasts and alternative scenarios for budgeting and decision making.

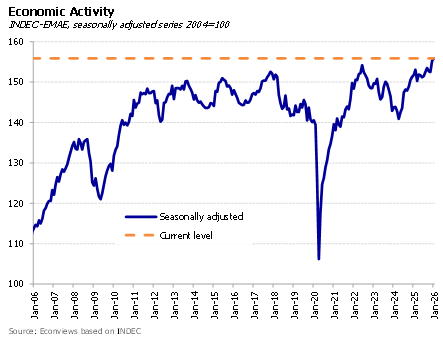

What the Data Says About Economic Activity. The debate over economic activity gained intensity following the publication of the 2025 Q4 GDP and the January EMAE (Monthly Estimator of Economic Activity), which showed that the aggregate economy is growing. In January, even lagging sectors such as industry and construction showed a monthly recovery. However, the trend reveals a more complex story: the most dynamic sectors are agriculture, energy, mining, fishing, and financial intermediation—all of which (except the latter) are more closely tied to exports than to the domestic market.

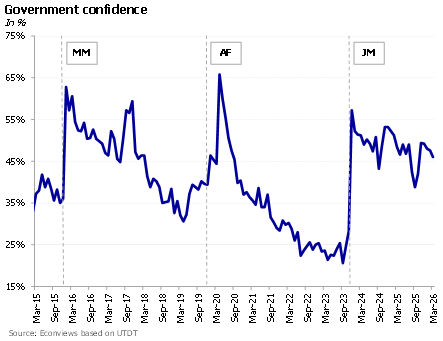

The government is facing a rapid deterioration in the political and social climate, just four months after the impressive electoral victory of last October. This has been particularly surprising because it is happening after having passed in Congress the long-awaited labor reform, which was expected to give a boost to the credibility of the program. But something went wrong.

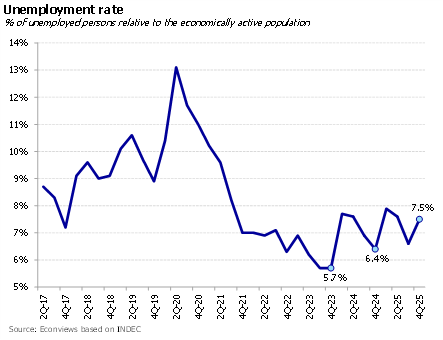

It is still too early to draw conclusions, but there are signs that the Government is shifting its monetary policy stance. Despite several officials doubling down in recent weeks to argue that the economy is growing and that jobs are not being lost, this week’s data and the policy decisions themselves challenge that narrative. The sense is that, even with inflation under pressure, the priority today is reactivation.

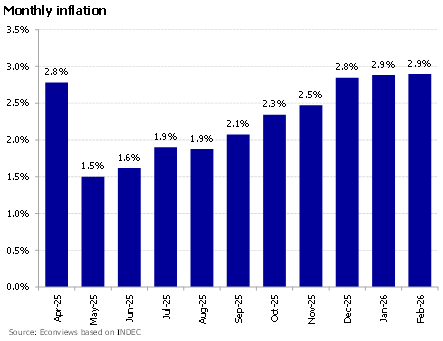

Preocupación por la inflación. El 2.9% mensual de febrero volvió a decepcionar, porque marcó el noveno mes en el que la inflación no baja y estuvo por encima de lo esperado por el mercado. El problema central es que el programa económico carece de un ancla nominal clara y las expectativas inflacionarias siguen ajustando para arriba. Marzo va a ser otro mes complicado: además de la usual estacionalidad alta, se suman los aumentos en combustibles y tarifas, y nuestro relevamiento de precios tampoco muestra una desaceleración en alimentos. La dinámica debería empezar a mejorar a partir de abril, pero la expectativa para este año es una inflación más cercana a 30% que al 20% que esperaba el mercado hace pocos meses.

Last week kicked off with high hopes around the Argentina Week in New York and ended on a sour note with the February inflation print. The timing for the event was far from ideal — the Government went out to sell the country to the world while investors had one eye glued to the Middle East. Even so, the event went ahead, significant investment announcements were made, and Argentina was back in the international spotlight, which is no small thing. On the home front, however, things were more complicated: inflation is showing no signs of deceleration, and consumption remains sluggish.

Más rápido de lo que muchos economistas esperaban, el Gobierno va consolidando su objetivo de cerrar el año con déficit fiscal cero, mejora de las cuentas del Banco Central, y camino a la tasa de inflación de un dígito porcentual….

Graduate in Economics from the University of Buenos Aires and Ph.D. in Economics from Columbia University. Professor and researcher at the Di Tella University and academic advisor at FIEL

With vast experience as an advisor to multilateral organizations such as the IMF, the World Bank and the Inter-American Development Bank, as well as several Latin American countries, he held prominent roles in the financial sector, including the presidency of Banco Hipotecario S.A. and functions in the Ministry of Economy and the Central Bank of the Argentine Republic.

He was an Assistant Professor at the University of Maryland, and taught at institutions such as CEMA, Georgetown University, and Columbia University.

He is a columnist and author of numerous articles in international publications. Author of the book “The Argentine economic crisis, a history of adjustments and imbalances” with Sebastián Kiguel.

Graduate in Economics from the University of Buenos Aires and MSc in Economics from the University of Warwick (UK).

He was an economic consultant at the Inter-American Development Bank (IDB) and at Econviews. He also served as an advisor at the Ministry of Economy and the Ministry of Transport of Argentina.