We offer reports on the Argentine economic and financial situation, focused on key aspects such as the level of activity, fiscal accounts, inflation, interest rates and exchange rates.

Presentations

We make in-company presentations on the Argentine and international economic situation, adjusting to the client's needs.

Consultations

We are available for specific queries from our clients on current issues via phone or email.

Forecasting

We prepare detailed long-term economic forecasts and alternative scenarios for budgeting and decision making.

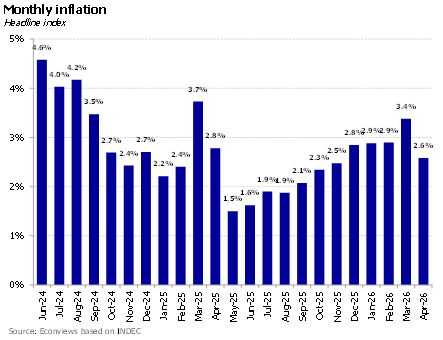

In April, inflation fell for the first time in 10 months. This is a positive figure considering it had been on the rise and reached 3.4% in March. There is no doubt that this figure was an isolated event because, beyond the ups and downs of recent months, inflation has maintained an average of around 2.5% over the last year and a half. This trend suggests that medium-term core or inertial inflation could be between 2.0% and 2.5% (probably closer to the lower bound), so we will have to see how monetary policy evolves to bring it under control.

Se extiende el efecto Fitch. Tras la suba de calificación de la semana pasada, el riesgo país comprimió unos 50 puntos hasta la zona de los 500, una mejora que se dio con el riesgo emergente relativamente estable, lo que achicó la brecha con otros países de alto riesgo. La onda verde se extendió porque desde Moody’s indicaron que también podrían mejorar el rating en los próximos meses. Con dos de las tres grandes calificadoras apuntando en la misma dirección, nuevos fondos quedarían habilitados para invertir en bonos argentinos. Se abre una nueva ventana para una emisión internacional con el riesgo país coqueteando nuevamente los 500 puntos, que, a nuestro criterio, sería muy positiva.

If we look at the regional country-risk rankings, Argentina is still the black sheep of Latin America. Despite the sharp improvement in sovereign spreads since Javier Milei took office — with country risk falling from nearly 2,000 basis points to around 515 today — Argentina remains near the bottom of the table, ahead only of Venezuela, which “relegated” (went to the B league) many years ago. Even countries that just months ago seemed headed for crisis, such as Bolivia and Ecuador, are now ahead of Argentina and have already returned to international debt markets. Can Argentina finally converge with the rest of the region?

Calma en el frente cambiario. El tipo de cambio sigue muy firme y se consolida nuevamente por debajo de los AR$ 1,400, casi 24% por debajo del techo de la banda, mientras el BCRA continúa comprando reservas. Esto ocurre a pesar de que la liquidación de la cosecha gruesa viene algo atrasada por las lluvias (promedio de US$ 138 millones diarios en los últimos 10 días, vs. US$ 196 millones del promedio histórico para la época), algo que debería empezar a corregirse durante mayo. Por el lado financiero también se esperan buenos flujos: en abril se emitieron unos US$ 1,700 millones entre ONs y bonos provinciales, a los que se suman las emisiones previstas para mayo (como los US$ 500 millones de CABA). Los préstamos en dólares crecieron con fuerza en abril (US$ 1,303 millones) y aportaron US$ 4,129 millones de oferta al MULC en los primeros cuatro meses del año. Tienen espacio para seguir creciendo, aunque las colocaciones MEP del Tesoro les restan algo de oferta. Con todo, esperamos que el tipo de cambio se mantenga firme y que el BCRA acelere el ritmo de compras en las próximas semanas. De todas formas, habrá que monitorear si el BCRA permite una combinación de tipo de cambio y compra de dólares algo más alta para evitar que la inflación erosione la competitividad, y si en algún momento (estimamos fines de junio) aumenta la presión cambiaria por cierre de posiciones en pesos antes de que merme la estacionalidad de la oferta del agro.

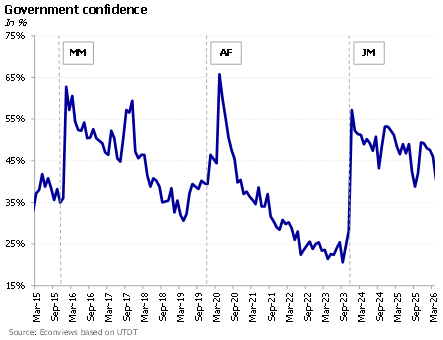

In recent months, the government has been facing setbacks on both the political and economic fronts that are affecting its positive image. The latest figures show a 12.1% drop in the Government Confidence Index published by Universidad Di Tella, marking the third consecutive decline. In addition, surveys from Universidad de San Andrés indicate that approval of Javier Milei’s administration continues to fall, dropping to 36% (down from 39% in March) while disapproval rose to 61%.

Más rápido de lo que muchos economistas esperaban, el Gobierno va consolidando su objetivo de cerrar el año con déficit fiscal cero, mejora de las cuentas del Banco Central, y camino a la tasa de inflación de un dígito porcentual….

Graduate in Economics from the University of Buenos Aires and Ph.D. in Economics from Columbia University. Professor and researcher at the Di Tella University and academic advisor at FIEL

With vast experience as an advisor to multilateral organizations such as the IMF, the World Bank and the Inter-American Development Bank, as well as several Latin American countries, he held prominent roles in the financial sector, including the presidency of Banco Hipotecario S.A. and functions in the Ministry of Economy and the Central Bank of the Argentine Republic.

He was an Assistant Professor at the University of Maryland, and taught at institutions such as CEMA, Georgetown University, and Columbia University.

He is a columnist and author of numerous articles in international publications. Author of the book “The Argentine economic crisis, a history of adjustments and imbalances” with Sebastián Kiguel.

Graduate in Economics from the University of Buenos Aires and MSc in Economics from the University of Warwick (UK).

He was an economic consultant at the Inter-American Development Bank (IDB) and at Econviews. He also served as an advisor at the Ministry of Economy and the Ministry of Transport of Argentina.