We offer reports on the Argentine economic and financial situation, focused on key aspects such as the level of activity, fiscal accounts, inflation, interest rates and exchange rates.

Presentations

We make in-company presentations on the Argentine and international economic situation, adjusting to the client's needs.

Consultations

We are available for specific queries from our clients on current issues via phone or email.

Forecasting

We prepare detailed long-term economic forecasts and alternative scenarios for budgeting and decision making.

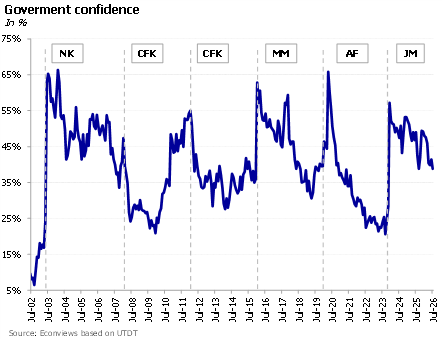

The World Cup is over and now the focus is once again on the economy, with an eye on next year’s election. On the political front, the government faces a mixed outlook. On the one hand, the index of confidence in the government published by Universidad Di Tella shows a drop of 6.5% in July, a worrisome figure, though on the other hand, it benefits from a divided opposition without a clear leader that can challenge Milei in the presidential election. The Peronist party is entangled in internal disputes between Cristina Kirchner and Axel Kicillof, while the moderate opposition (including moderate Peronists, radicals, and former PRO) cannot get its act together. True, the elections are a year away and many things can happen along the way, but for the moment the government seems to be leading the opinion polls.

Milei, in a show of pragmatism, decided to keep the Central Bank open and grant it independence from political power. He also announced that he will introduce a new law to develop the capital markets and another to reform the insurance market. These are three initiatives that, in principle, point in the right direction. The problem is that, at least for now, much of that thinking is not yet reflected in the Government’s own practice.

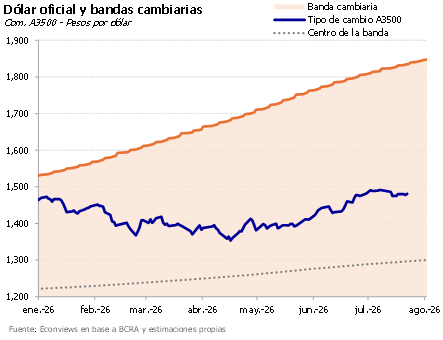

Dólar picante. El tipo de cambio volvió al centro de la escena y el martes se acercó a los AR$1,500, cortando la racha de 135 ruedas consecutivas con saldo comprador del BCRA en el MULC. Como viene pasando en los últimos meses, el tipo de cambio tiende a presionar los días en que se fija el precio de las letras dollar linked, y el martes no fue la excepción, aunque esta vez hizo falta más intervención para contener la suba (trascendió que el Tesoro habría vendido dólares spot). Más allá de este evento puntual, ayer el dólar retrocedió un poco y el BCRA compró US$ 36 millones. En la licitación de ayer el Tesoro absorbió unos AR$ 3.7 billones, mientras que la liquidez excedente rondaba los AR$ 2 billones, así que las tasas podrían tensarse si es que no hubo inyección de pesos por otra vía. Queda claro que al Gobierno no le resulta cómodo un dólar arriba de AR$ 1,500. Nuestro escenario sigue más cerca del dólar Ravier de AR$ 1,800 para fin de año.

Volatility persists in international markets, with oil flirting again with the $100-a-barrel mark, and long-term rates back at their highest levels of the year on fears that inflation will pick up. This combination weighed on almost every emerging market, which saw exchange rates rise and country risk premiums widen, two factors that also affected Argentina. We live in a context where external conditions change almost daily.

Sigue la calma en el dólar. Fue otra semana tranquila para el tipo de cambio, que se mantuvo en el rango de AR$ 1,480. La novedad es que bajó considerablemente el volumen operado en títulos dollar linked, lo que sugiere que cedió un poco la presión cambiaria y el gobierno necesitó vender menos cobertura para sostener el tipo de cambio. De todos modos, parte de la demanda de cobertura se había canalizado mediante la licitación de deuda de la semana pasada, donde se colocaron unos US$ 967 millones de bonos dollar linked. Lo que sí subió es la brecha entre el contado con liqui y el MEP a más de 4%. No descartamos que la presión sobre el tipo de cambio vuelva a aparecer.

Más rápido de lo que muchos economistas esperaban, el Gobierno va consolidando su objetivo de cerrar el año con déficit fiscal cero, mejora de las cuentas del Banco Central, y camino a la tasa de inflación de un dígito porcentual….

Graduate in Economics from the University of Buenos Aires and Ph.D. in Economics from Columbia University. Professor and researcher at the Di Tella University and academic advisor at FIEL

With vast experience as an advisor to multilateral organizations such as the IMF, the World Bank and the Inter-American Development Bank, as well as several Latin American countries, he held prominent roles in the financial sector, including the presidency of Banco Hipotecario S.A. and functions in the Ministry of Economy and the Central Bank of the Argentine Republic.

He was an Assistant Professor at the University of Maryland, and taught at institutions such as CEMA, Georgetown University, and Columbia University.

He is a columnist and author of numerous articles in international publications. Author of the book “The Argentine economic crisis, a history of adjustments and imbalances” with Sebastián Kiguel.

Graduate in Economics from the University of Buenos Aires and MSc in Economics from the University of Warwick (UK).

He was an economic consultant at the Inter-American Development Bank (IDB) and at Econviews. He also served as an advisor at the Ministry of Economy and the Ministry of Transport of Argentina.