We offer reports on the Argentine economic and financial situation, focused on key aspects such as the level of activity, fiscal accounts, inflation, interest rates and exchange rates.

Presentations

We make in-company presentations on the Argentine and international economic situation, adjusting to the client's needs.

Consultations

We are available for specific queries from our clients on current issues via phone or email.

Forecasting

We prepare detailed long-term economic forecasts and alternative scenarios for budgeting and decision making.

Volatility persists in international markets, with oil flirting again with the $100-a-barrel mark, and long-term rates back at their highest levels of the year on fears that inflation will pick up. This combination weighed on almost every emerging market, which saw exchange rates rise and country risk premiums widen, two factors that also affected Argentina. We live in a context where external conditions change almost daily.

Sigue la calma en el dólar. Fue otra semana tranquila para el tipo de cambio, que se mantuvo en el rango de AR$ 1,480. La novedad es que bajó considerablemente el volumen operado en títulos dollar linked, lo que sugiere que cedió un poco la presión cambiaria y el gobierno necesitó vender menos cobertura para sostener el tipo de cambio. De todos modos, parte de la demanda de cobertura se había canalizado mediante la licitación de deuda de la semana pasada, donde se colocaron unos US$ 967 millones de bonos dollar linked. Lo que sí subió es la brecha entre el contado con liqui y el MEP a más de 4%. No descartamos que la presión sobre el tipo de cambio vuelva a aparecer.

Cambió la dinámica del mercado de pesos. Desde junio, el mercado de pesos se viene comportando distinto. Por un lado, hay menos emisión vinculada a la compra de dólares del BCRA porque el ritmo de compras se redujo a la mitad (al menos hasta antes de esta semana). Al mismo tiempo, la venta de bonos dollar linked por parte del Central para contener la brecha absorbe pesos. Todo esto hace que la liquidez esté un poco más ajustada. En la licitación de hace dos semanas, el Tesoro soltó pesos y compensó esa caída de liquidez, pero a medida que pasaron los días el efecto se fue esfumando. Las tasas cortas amagaron con subir esta semana a niveles de 21.5%, pero inferimos que el Tesoro o el Central salieron a operar en el secundario para dar liquidez y bajarlas. Esto confirma que la estrategia del Gobierno sigue siendo mantener tasas bajas y administrar la presión cambiaria vendiendo cobertura.

The Government has announced its proposal to reform the Central Bank’s Charter, and although we do not yet know the fine print of the bill to be sent to Congress, everything indicates it is a positive step. The law proposes, among other things, the independence of the Central Bank and the elimination of monetary issuance to finance the Treasury. This shows that the project seeks to improve institutional quality and to focus the Central Bank on its primary task: working to achieve price stability.

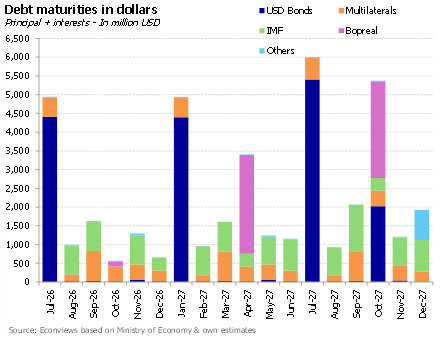

A reasonable financial program. The economic team presented the financial program, something not seen since the Dujovne era, taking a positive step toward gaining predictability over next year’s maturities and clearing uncertainty ahead of an election year. Broadly speaking, we find it reasonable and quite in line with our numbers: the Government plans to issue at least USD 5 billion in the local market and add another USD 2 billion from other loans, on top of the USD 3.7 billion in overfinancing that will carry over from this year. In addition, the Treasury will have to purchase around USD 5 billion from the BCRA to cover the gap. These are achievable goals, but not without risks, considering it will be an election year with portfolio dollarization, which could complicate both the BCRA’s effort to accumulate reserves and the Treasury’s ability to issue debt. For more detail, see the note below.

Más rápido de lo que muchos economistas esperaban, el Gobierno va consolidando su objetivo de cerrar el año con déficit fiscal cero, mejora de las cuentas del Banco Central, y camino a la tasa de inflación de un dígito porcentual….

Graduate in Economics from the University of Buenos Aires and Ph.D. in Economics from Columbia University. Professor and researcher at the Di Tella University and academic advisor at FIEL

With vast experience as an advisor to multilateral organizations such as the IMF, the World Bank and the Inter-American Development Bank, as well as several Latin American countries, he held prominent roles in the financial sector, including the presidency of Banco Hipotecario S.A. and functions in the Ministry of Economy and the Central Bank of the Argentine Republic.

He was an Assistant Professor at the University of Maryland, and taught at institutions such as CEMA, Georgetown University, and Columbia University.

He is a columnist and author of numerous articles in international publications. Author of the book “The Argentine economic crisis, a history of adjustments and imbalances” with Sebastián Kiguel.

Graduate in Economics from the University of Buenos Aires and MSc in Economics from the University of Warwick (UK).

He was an economic consultant at the Inter-American Development Bank (IDB) and at Econviews. He also served as an advisor at the Ministry of Economy and the Ministry of Transport of Argentina.