Reports

When the Government unexpectedly swept last year’s midterm elections, it seemed that in 2026 it would take the world by storm. The wave of optimism suggested it would consolidate its popularity, advance forcefully in Congress, and — with the “kuka” (left-populist) risk cleared — that the arrival of investment would accelerate. On the economic front, the program was expected to start showing more decisive results in activity and disinflation once the electoral shock had passed. Six months later, the balance is more mixed. There were important achievements, some stumbles, and a political agenda that got more complicated than expected.

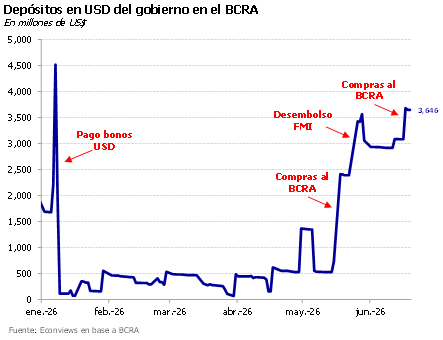

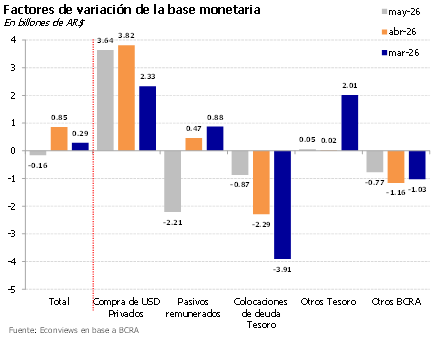

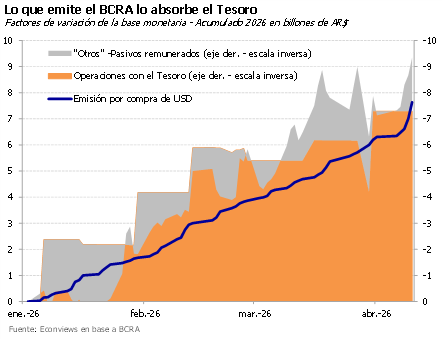

Sigue la presión cambiaria. El tipo de cambio oficial cerró ayer en AR$ 1,490 y retomó la suba después de unos días de relativa calma, en los que tuvo mucho que ver el Banco Central profundizando la venta de títulos dollar linked para contener la suba. Estimamos que el BCRA también estuvo activo en futuros, donde el interés abierto subió casi US$ 600 millones en junio. La idea del Gobierno parece ser evitar movimientos abruptos que generen nerviosismo. Lo positivo es que el BCRA sigue comprando en el mercado de cambios, aunque a un ritmo bastante menor que en los últimos meses. Esperamos que la tendencia alcista del dólar continúe.

After months of turbulence, the Argentine economy has entered a calmer financial period. Inflation has begun to fall, interest rates have remained at around 20% for a few months after a period of erratic movement, and the EMBI has dropped significantly. The exception has been some recent move in the exchange rate, though this looks like a welcome outcome to avoid further real appreciation of the currency.

There’s no doubt that the wind has shifted in the foreign exchange market. The exchange rate rose almost 5% in June, breaking a stability that had lasted more than five months. It’s not a worrying increase, but it clearly shows that the second half of the year will be more challenging on this front. It is also the first real test the Government has faced since the reserve accumulation program began and since monetary policy adopted an expansionary bias.

El dólar sigue subiendo y el BCRA empieza a vender futuros. El tipo de cambio oficial cerró ayer en AR$ 1,479 y acumula una suba de 4.9% en junio. Parte de la presión viene del contexto externo con el dólar que se fortaleció a nivel global y el real cayendo más de 2% en la última semana. El mercado de futuros tuvo su mayor salto de interés abierto desde septiembre (US$ 224 millones en un día), lo que sugiere que el BCRA estuvo vendiendo contratos para contener la presión. En mayo el Central había reducido su posición vendedora a casi cero, así que tiene margen para seguir operando. En el contado, en cambio, las compras cayeron a mínimos desde marzo. Lejos de preocuparnos, la suba del tipo de cambio nos parece positiva. De todos modos, es probable que el BCRA profundice la venta de futuros y dollar linked si la presión continúa.

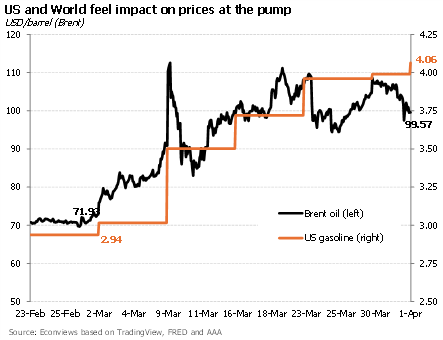

While all eyes are on the World Cup, there were other important developments last week coming from the United States. On one hand, after three months of war, a preliminary agreement was reached to end the conflict and reopen the Strait of Hormuz. Peace still looks fragile and considerable volatility is expected during the 60 days that the negotiations are set to last, but the concrete fact is that oil has already fallen to the USD 80-per-barrel range. This is good news for inflation, although not quite as good for our exports.

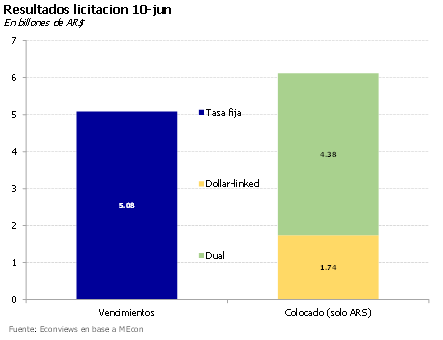

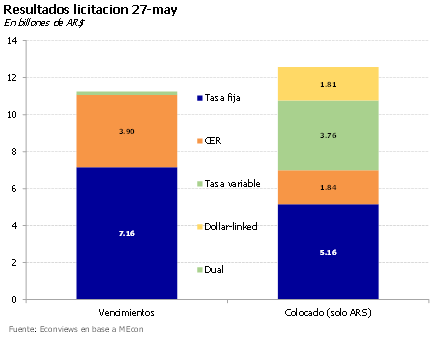

Persiguiendo a Ecuador. El riesgo país comprimió unos 70 puntos desde que el miércoles pasado Standard and Poor’s mejoró la calificación de la deuda argentina en dólares de CCC+ a B-. Hace un mes Fitch había hecho lo mismo, y probablemente Moody’s lo haga pronto también. Con dos de las tres big three ubicando a Argentina en B-, se amplía el abanico de fondos que pueden comprar bonos argentinos. Eso impulsó la baja del riesgo país hasta la zona de 430 puntos, achicando la brecha con Ecuador, que está en 390. Esta semana también se conoció que el Banco Mundial aprobó el esquema de garantías para acceder a financiamiento por US$ 2,000 millones. De a poco se va completando el programa financiero, pero seguimos pensando que una colocación internacional abriría un círculo virtuoso que permitiría bajar más el riesgo país y financiarse a mejores tasas. Esperamos que el gobierno se anime más adelante este año.

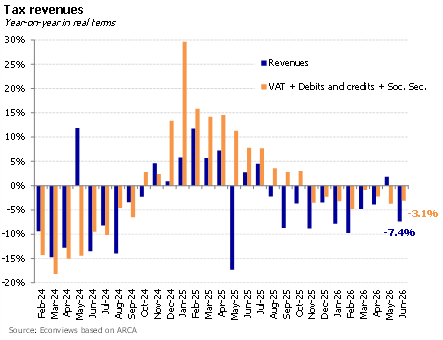

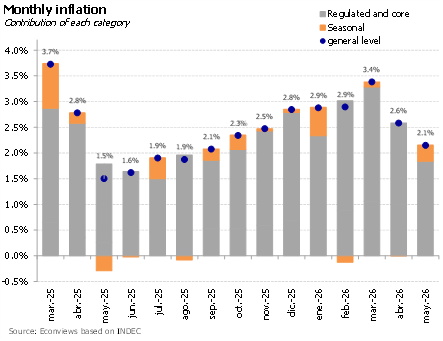

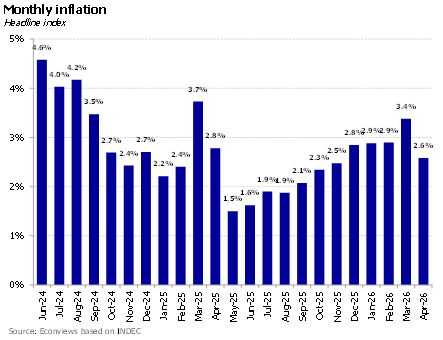

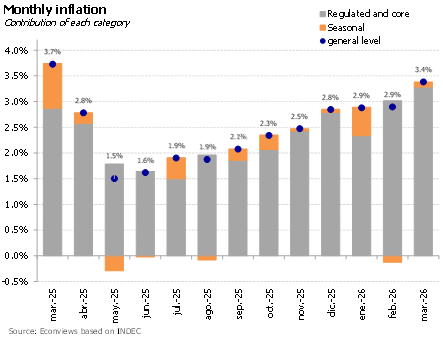

Last week’s economic news brought two reasons for relief. On the one hand, inflation fell again, confirming that the slowdown continues and that the high inflation rates seen during the summer were a passing phenomenon. Our estimates for high-frequency food inflation are encouraging, although, just as there was no reason to be alarmed by the data from recent months, there is also not enough evidence to assert that inflation that has been above 2.0% monthly for more than 18 months is now under control. It is very likely that inflationary inertia will continue, albeit with a downward trend

Primero Fitch, ahora S&P. La calificadora Standard and Poor’s mejoró la deuda argentina en dólares de CCC+ a B-, un mes después de que Fitch hiciera lo mismo. La reclasificación pone a Argentina en la liga de Ecuador, que hace poco emitió 1,000 millones al 8.5% en su segunda colocación del año.

Se despertó el dólar en junio. Luego de un inicio de año donde el tipo de cambio oficial había estado muy tranquilo (incluso con periodos de apreciación nominal), empezó a verse algo más de movimiento. En mayo cerró 2.1% arriba punta a punta contra abril y en las primeras 3 rondas de junio ya aumentó 1.8% contra el cierre de mayo. El CCL quedó en AR$ 1,514. Vemos como algo positivo que el dólar empiece a moverse a un ritmo parecido al de la inflación para evitar que se siga apreciando en términos reales. Sobre todo, si se da en una forma suave como en estos meses. En nuestro escenario base seguimos viendo un tipo de cambio que se mueve más rápido en el segundo semestre, aunque todavía quedando lejos de la banda superior.

Suben las tasas de interés en el mundo. La guerra en medio Oriente tuvo víctimas económicas: más inflación y subas en las tasas de interés. El bono del Tesoro de EEUU a 30 años tocó esta semana 5.18%, un máximo desde 2007, mientras que la de 10 años subió a la zona de 4.60%. El tramo largo de la curva impacta directamente en la tasa de hipotecas y en los bonos de largo plazo. Mala noticia para los países emergentes, dado que el costo de endeudamiento aumenta por lo menos medio punto porcentual. Además, disminuyen las chances de que la Fed, que desde mañana va a ser presidida por Kevin Warsh, baje las tasas de corto plazo este año. Warsh no la tiene fácil. Su primera comunicación será mañana mismo y el mercado espera ver si le imprime un sesgo contractivo en un contexto donde la inflación está presionada por la guerra. Hay que estar alerta, porque si se profundiza el giro hacia tasas más altas habrá impacto en bolsas, monedas y flujos a emergentes.

El dólar toma algo de impulso. Al cierre de ayer el tipo de cambio de referencia quedó en AR$ 1,411.2, subiendo 2.2% en lo que va del mes. Nos parece saludable que el dólar empiece a moverse a un ritmo parecido al de la inflación para evitar que se siga apreciando en términos reales. A pesar de esta leve suba, todavía está un 25% por debajo del techo de la banda, lo que le da espacio para que se mueva durante el segundo semestre, tal como esperamos en nuestro escenario base. La oferta en el mercado se mantiene alta, con el agro liquidando en promedio US$ 138 millones en los últimos 10 días. Tomando como referencia las campañas anteriores el ritmo de liquidación podría ser todavía mayor en esta época del año. Por eso esperamos que el flujo se mantenga, aunque habrá que ver cuánto de la liquidación del agro se queda en pesos. Los préstamos en dólares también siguen creciendo y complementan la oferta.

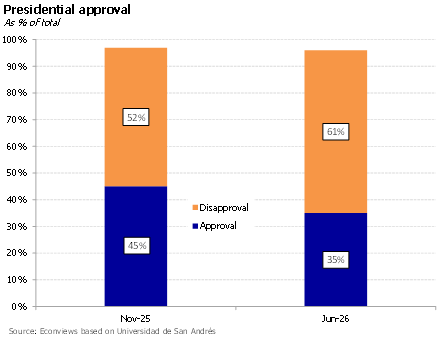

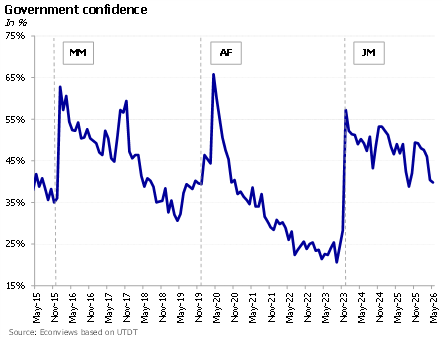

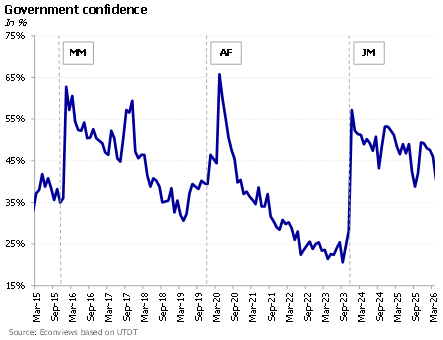

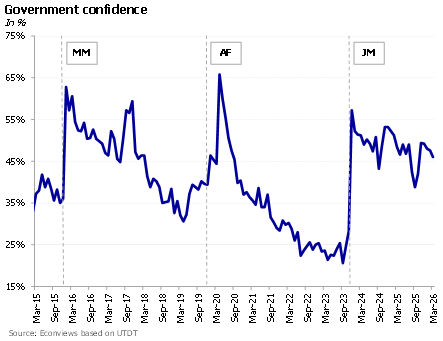

After a few difficult months, the economy is beginning to show signs of recovery, though this improvement is not yet reflected in the president’s image. The Government Confidence Index from Universidad Torcuato Di Tella fell 1.6% in May, marking six consecutive months of decline. At the same time, data from Universidad de San Andrés shows that presidential approval has dropped from 45% in November 2025 to 37% in May 2026. These are still reasonable numbers for a government that has been implementing an adjustment program for two and a half years. The administration does not feel under pressure so far, as there is no opposition figure capable of capitalizing on its difficulties. Peronism remains fragmented and lacks a clear leader, Macri orbits around but does not appear to have enough votes, and Bullrich distances herself from the ruling party without yet offering a clear alternative. The consensus among political analysts is that if an election were held today, Milei would win.

Country risk is falling again. This is undoubtedly partly thanks to the Central Bank’s purchases in the foreign exchange market, which are strengthening international reserves, partly because the credit rating was raised to B- by Fitch, and positive news is expected soon from Moody’s and eventually S&P. It’s also partly because the government has shown pragmatism in covering its financial needs by issuing dollar-denominated bonds in the local market, taking advantage of the foreign exchange supply.

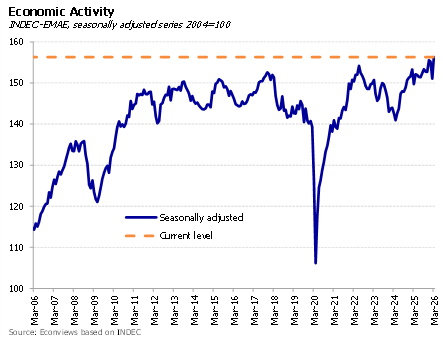

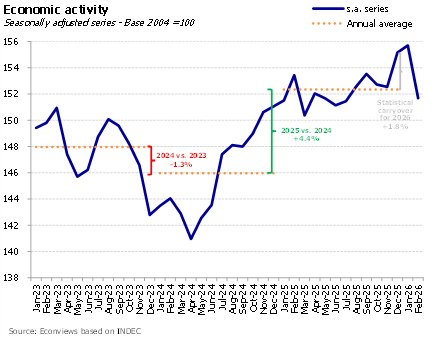

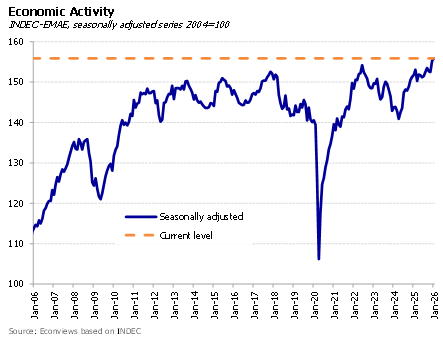

After several weeks of deteriorating economic indicators, a series of recent news and data give reasons for optimism. The latest economic activity figures show a 3.5% rebound in March, exports broke records with agriculture and energy products soaring, consumer confidence stopped falling and even saw a slight increase, private sector employment showed signs of life after eight months of decline, and the second review of the agreement with the IMF was approved. Furthermore, April’s inflation showed its first slowdown in ten months, and all indications are that it will continue to ease in May. After March closed with 3.4% inflation and February saw a sharp drop in activity, the new data is quite promising.

In April, inflation fell for the first time in 10 months. This is a positive figure considering it had been on the rise and reached 3.4% in March. There is no doubt that this figure was an isolated event because, beyond the ups and downs of recent months, inflation has maintained an average of around 2.5% over the last year and a half. This trend suggests that medium-term core or inertial inflation could be between 2.0% and 2.5% (probably closer to the lower bound), so we will have to see how monetary policy evolves to bring it under control.

Se extiende el efecto Fitch. Tras la suba de calificación de la semana pasada, el riesgo país comprimió unos 50 puntos hasta la zona de los 500, una mejora que se dio con el riesgo emergente relativamente estable, lo que achicó la brecha con otros países de alto riesgo. La onda verde se extendió porque desde Moody’s indicaron que también podrían mejorar el rating en los próximos meses. Con dos de las tres grandes calificadoras apuntando en la misma dirección, nuevos fondos quedarían habilitados para invertir en bonos argentinos. Se abre una nueva ventana para una emisión internacional con el riesgo país coqueteando nuevamente los 500 puntos, que, a nuestro criterio, sería muy positiva.

If we look at the regional country-risk rankings, Argentina is still the black sheep of Latin America. Despite the sharp improvement in sovereign spreads since Javier Milei took office — with country risk falling from nearly 2,000 basis points to around 515 today — Argentina remains near the bottom of the table, ahead only of Venezuela, which “relegated” (went to the B league) many years ago. Even countries that just months ago seemed headed for crisis, such as Bolivia and Ecuador, are now ahead of Argentina and have already returned to international debt markets. Can Argentina finally converge with the rest of the region?

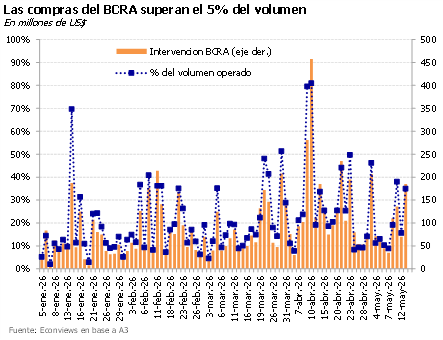

Calma en el frente cambiario. El tipo de cambio sigue muy firme y se consolida nuevamente por debajo de los AR$ 1,400, casi 24% por debajo del techo de la banda, mientras el BCRA continúa comprando reservas. Esto ocurre a pesar de que la liquidación de la cosecha gruesa viene algo atrasada por las lluvias (promedio de US$ 138 millones diarios en los últimos 10 días, vs. US$ 196 millones del promedio histórico para la época), algo que debería empezar a corregirse durante mayo. Por el lado financiero también se esperan buenos flujos: en abril se emitieron unos US$ 1,700 millones entre ONs y bonos provinciales, a los que se suman las emisiones previstas para mayo (como los US$ 500 millones de CABA). Los préstamos en dólares crecieron con fuerza en abril (US$ 1,303 millones) y aportaron US$ 4,129 millones de oferta al MULC en los primeros cuatro meses del año. Tienen espacio para seguir creciendo, aunque las colocaciones MEP del Tesoro les restan algo de oferta. Con todo, esperamos que el tipo de cambio se mantenga firme y que el BCRA acelere el ritmo de compras en las próximas semanas. De todas formas, habrá que monitorear si el BCRA permite una combinación de tipo de cambio y compra de dólares algo más alta para evitar que la inflación erosione la competitividad, y si en algún momento (estimamos fines de junio) aumenta la presión cambiaria por cierre de posiciones en pesos antes de que merme la estacionalidad de la oferta del agro.

In recent months, the government has been facing setbacks on both the political and economic fronts that are affecting its positive image. The latest figures show a 12.1% drop in the Government Confidence Index published by Universidad Di Tella, marking the third consecutive decline. In addition, surveys from Universidad de San Andrés indicate that approval of Javier Milei’s administration continues to fall, dropping to 36% (down from 39% in March) while disapproval rose to 61%.

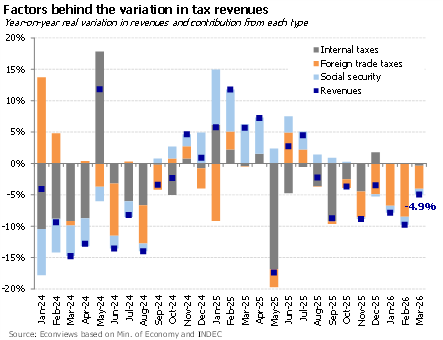

Investors are watching Argentina cautiously. After two weeks under pressure, sovereign bonds turned green again and country risk dropped to around 550 basis points. The previous rise had gone against the trend in other emerging markets and came amid rumors of a possible operation with the World Bank and the IDB to guarantee bank loans. This was compounded by very weak economic activity data and a decline in polling numbers (confidence in the government fell 12.1% in March, and surveys such as those by Universidad de San Andrés and AtlasIntel-Bloomberg show a deterioration in the government’s image). All of this heightened investor concerns about the sustainability of the economic program at a time when the electoral calendar is already starting to come into focus.

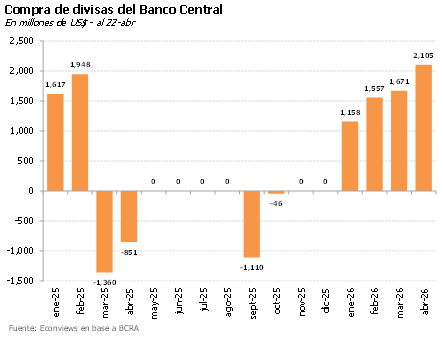

Se aceleran las compras del BCRA. Con seis días hábiles por delante, abril ya se posiciona como el mes con mayor compra de dólares del año, superando los US$ 2,100 millones. El buen desempeño se explica, por un lado, por el saldo positivo de la balanza comercial, impulsada por exportaciones que crecen e importaciones que aún no recuperan el ritmo previo a las elecciones (el INDEC informó esta semana un superávit de US$ 2,500 millones en marzo), y esto sin capturar aun plenamente la mejora en los términos de intercambio derivada de la guerra. Por otro lado, siguen jugando a favor los flujos financieros y según el BCRA, todavía quedan ingresar unos US$ 3,000 millones de ONs, a lo que se suman los préstamos en dólares que crecen a un ritmo de US$ 1,000 millones por mes. Con este panorama, y la liquidación de divisas del agro empezando a acelerar, esperamos que el Central siga con la racha compradora en los próximos meses.

The data are becoming increasingly clear and are beginning to speak for themselves, pointing to a “two-speed” or bipolar economy. The problem for the government is that the sustainability of the program depends on growth reaching a broad share of the population. Instead, what we are seeing is that the winners so far are a handful of sectors—mining, energy, and agriculture—which do not generate much employment. The losers—construction, manufacturing, and services, which are the main job creators—are stagnating or contracting. Employment and wages are not driving growth, and mass consumption is suffering, as reflected in the sharp decline in the consumer confidence index and in some surveys on the government’s approval ratings.

Javier Milei’s economic program is going through a critical moment. Inflation has risen over the past 10 months, reaching a peak of 3.4% monthly in March. At the same time, there are clear signs of stagnation—or even contraction—in industrial production, construction, mass consumption, and employment. Wages have been consistently losing ground to inflation, resulting in a steady erosion of purchasing power. The consequence, visible in recent months, is a decline in government approval, with polls showing Milei’s negative image now exceeding 50%.

Pasó lo peor para la inflación. El dato de marzo fue de 3.4%, en línea con lo que anticipábamos en Econviews. Las principales alzas se registraron en educación (típico de marzo), alimentos (3.4%, con fuerte incidencia de la carne) y restaurantes y comidas fuera del hogar. La suba de combustibles también dejó huella, aunque estimamos que parte de ese efecto se trasladará a abril. De todos modos, nuestro relevamiento de precios online muestra una desaceleración marcada en las últimas dos semanas: los alimentos pasaron de correr al 3.4% mensual al 2.4%, en un contexto donde los aumentos en precios regulados también se moderaron. Para abril esperamos una desaceleración hacia el 2.7%.

After years of rollercoaster mode, the Argentine economy has entered a less dizzying phase. Weekly shocks and abrupt shifts in sentiment have subsided, which is, in itself, good news. Within this framework of greater stability, February and March will likely stand out as the weakest months of the year in terms of activity and inflation.

Strong purchases in the first quarter. In recent days, the Central Bank stepped on the accelerator and closed the first quarter with foreign exchange purchases exceeding USD 4.3 billion, at a pace of nearly USD 1.5 billion per month. With the start of the main harvest season, the Central Bank now has the opportunity to deepen this pace and complete an even stronger second quarter, moving closer to the US$ 10 billion target for the year. Net reserves improved, although they remain in negative territory due to debt payments and the drop in gold prices.

What the Data Says About Economic Activity. The debate over economic activity gained intensity following the publication of the 2025 Q4 GDP and the January EMAE (Monthly Estimator of Economic Activity), which showed that the aggregate economy is growing. In January, even lagging sectors such as industry and construction showed a monthly recovery. However, the trend reveals a more complex story: the most dynamic sectors are agriculture, energy, mining, fishing, and financial intermediation—all of which (except the latter) are more closely tied to exports than to the domestic market.

The government is facing a rapid deterioration in the political and social climate, just four months after the impressive electoral victory of last October. This has been particularly surprising because it is happening after having passed in Congress the long-awaited labor reform, which was expected to give a boost to the credibility of the program. But something went wrong.