Reports

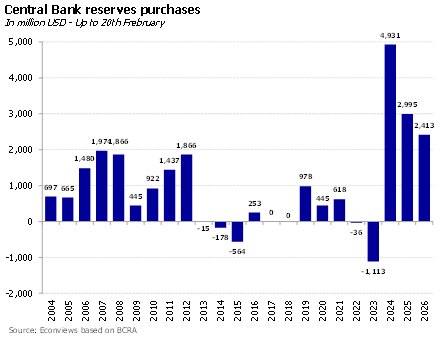

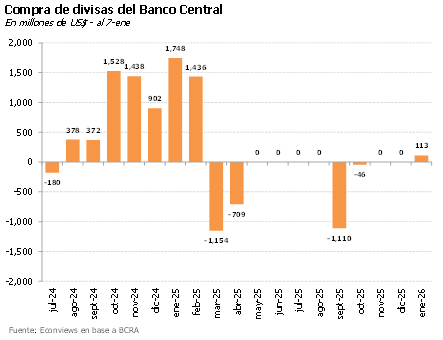

Strong purchases in the first quarter. In recent days, the Central Bank stepped on the accelerator and closed the first quarter with foreign exchange purchases exceeding USD 4.3 billion, at a pace of nearly USD 1.5 billion per month. With the start of the main harvest season, the Central Bank now has the opportunity to deepen this pace and complete an even stronger second quarter, moving closer to the US$ 10 billion target for the year. Net reserves improved, although they remain in negative territory due to debt payments and the drop in gold prices.

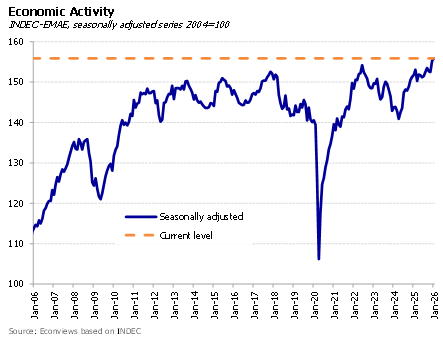

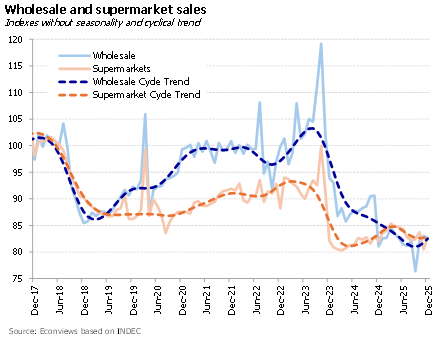

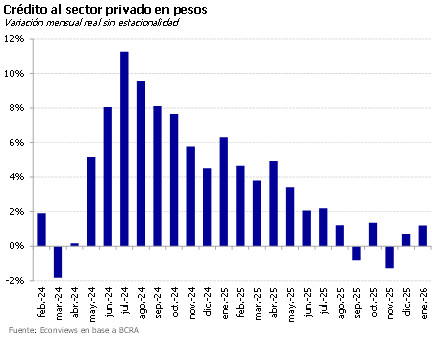

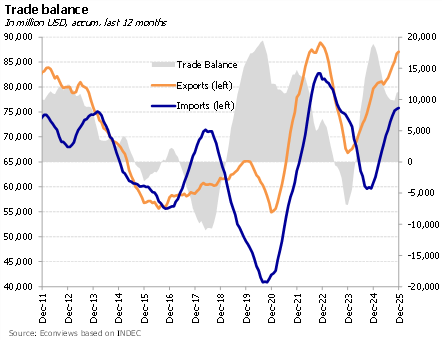

What the Data Says About Economic Activity. The debate over economic activity gained intensity following the publication of the 2025 Q4 GDP and the January EMAE (Monthly Estimator of Economic Activity), which showed that the aggregate economy is growing. In January, even lagging sectors such as industry and construction showed a monthly recovery. However, the trend reveals a more complex story: the most dynamic sectors are agriculture, energy, mining, fishing, and financial intermediation—all of which (except the latter) are more closely tied to exports than to the domestic market.

The government is facing a rapid deterioration in the political and social climate, just four months after the impressive electoral victory of last October. This has been particularly surprising because it is happening after having passed in Congress the long-awaited labor reform, which was expected to give a boost to the credibility of the program. But something went wrong.

It is still too early to draw conclusions, but there are signs that the Government is shifting its monetary policy stance. Despite several officials doubling down in recent weeks to argue that the economy is growing and that jobs are not being lost, this week’s data and the policy decisions themselves challenge that narrative. The sense is that, even with inflation under pressure, the priority today is reactivation.

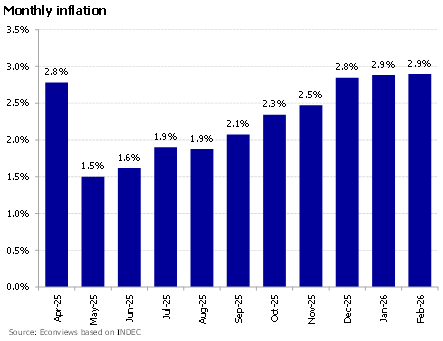

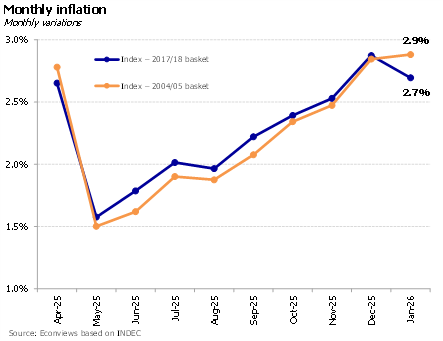

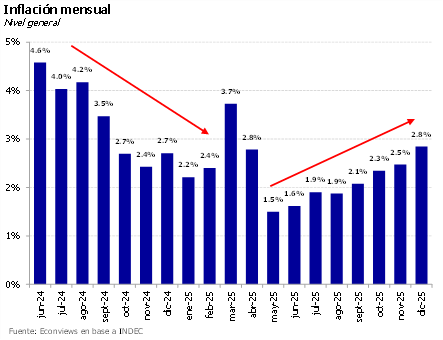

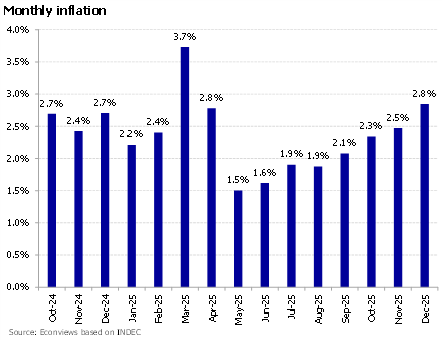

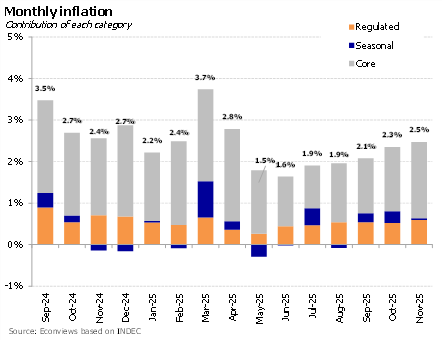

Preocupación por la inflación. El 2.9% mensual de febrero volvió a decepcionar, porque marcó el noveno mes en el que la inflación no baja y estuvo por encima de lo esperado por el mercado. El problema central es que el programa económico carece de un ancla nominal clara y las expectativas inflacionarias siguen ajustando para arriba. Marzo va a ser otro mes complicado: además de la usual estacionalidad alta, se suman los aumentos en combustibles y tarifas, y nuestro relevamiento de precios tampoco muestra una desaceleración en alimentos. La dinámica debería empezar a mejorar a partir de abril, pero la expectativa para este año es una inflación más cercana a 30% que al 20% que esperaba el mercado hace pocos meses.

Last week kicked off with high hopes around the Argentina Week in New York and ended on a sour note with the February inflation print. The timing for the event was far from ideal — the Government went out to sell the country to the world while investors had one eye glued to the Middle East. Even so, the event went ahead, significant investment announcements were made, and Argentina was back in the international spotlight, which is no small thing. On the home front, however, things were more complicated: inflation is showing no signs of deceleration, and consumption remains sluggish.

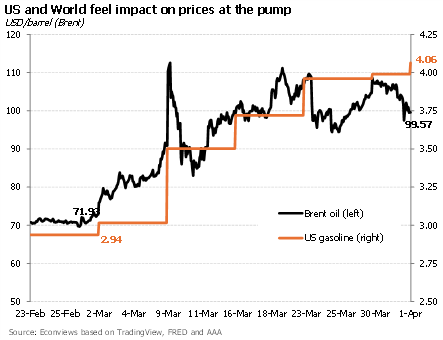

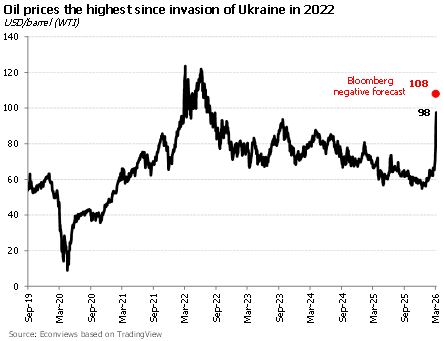

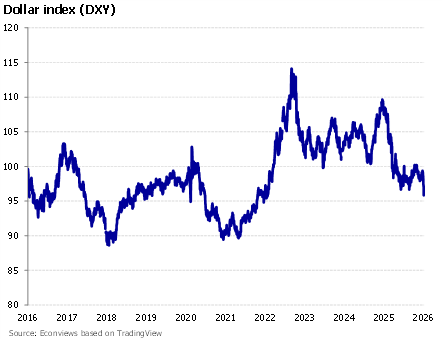

¿Shock transitorio o permanente? Los mercados globales siguen operando con alta volatilidad por el conflicto con Irán. El escenario base que descuentan los mercados es que el shock será transitorio, pero crece la probabilidad de que el conflicto derive en un precio del petróleo elevado por más tiempo, lo que pondría a la Reserva Federal ante un dilema entre combatir una inflación más alta y sostener un mercado laboral que se debilita. Lo que parece claro es que el petróleo no volverá rápidamente a los niveles previos al conflicto, ya que restablecer las cadenas de suministro en Medio Oriente llevará tiempo. Europa y Asia son las regiones más afectadas. El dólar operó algo más débil en los últimos días y las tasas no mostraron saltos significativos.

The war in the Middle East has put the brakes on the very favorable international environment that the Argentine economy had been riding. Through February, global markets were showing a strong appetite for risk assets and the dollar was weakening, which was pushing up emerging market currencies and compressing credit spreads to levels not seen in years.

El conflicto en medio oriente domina los mercados. La escalada bélica le puso fin a la racha de dólar débil y baja de riesgo emergente que venía dando viento de cola para argentina en 2026. En este contexto, el peso y el riesgo país operaron bajo presión, en sintonía con sus pares globales, aunque sin movimientos extremos. La clave será el factor tiempo. Si el conflicto se prolonga y recalienta los precios de la energía y los commodities, la inflación en EE. UU. podría forzar a la Fed a un sendero de tasas altas por más tiempo, cerrando la canilla de flujos hacia emergentes. Si se resuelve rápido, el shock habrá sido solo un susto pasajero.

The labor reform shows the determination of the Milei administration to advance structural reforms that can improve the business environment. It also shows that he has achieved a political consolidation in Congress. We expect that this reform will be quickly followed by others, namely the law of glaciers and a tax reform, and by numerous decrees to continue the deregulation of the economy.

Taking advantage of a relatively quiet local macro environment, we turned our focus toward the global front. In just one week: IBM suffered its worst stock market decline in 26 years, a profitable digital payments company laid off 40% of its workforce, and a hypothetical report on mass unemployment went viral on Wall Street. The common thread was neither a financial crisis nor a recession: it was Artificial Intelligence. What until recently was a debate about the future of work is turning into a series of concrete and measurable facts. The question is no longer whether this technological revolution will have a macroeconomic impact, but how deep it will be and how fast it will arrive.

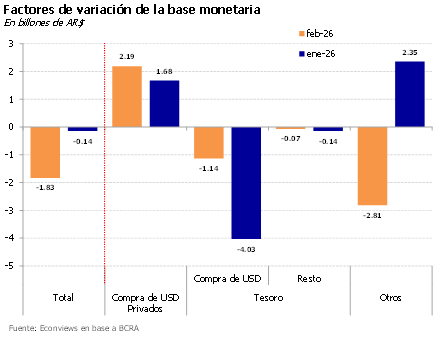

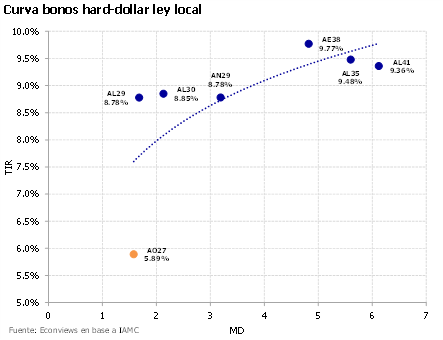

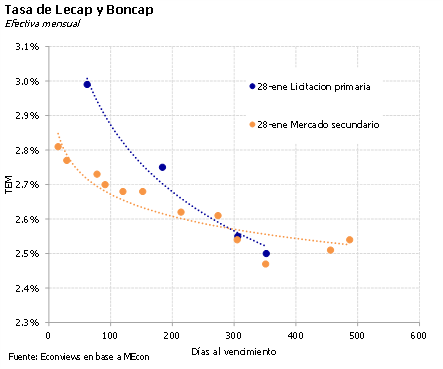

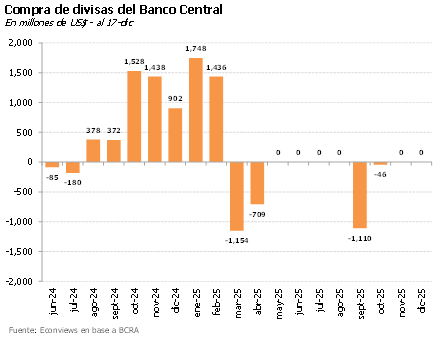

El BCRA sigue comprando y el Tesoro anuncia cómo va a pagar julio. Con compras acumuladas en 2026 que ya superan los US$ 2,600 millones en 36 ruedas consecutivas, la novedad de la semana fue el lanzamiento del Bonar 2027. El Tesoro comenzó a licitar un bono hard-dollar ley local con cupón del 6% e intereses mensuales, buscando captar hasta US$ 2,000 millones en licitaciones quincenales para pre-financiar los vencimientos de julio, que ascienden a cerca de US$ 4,200 millones entre capital e intereses. En la primera subasta de ayer, la demanda fue de casi US$ 900 millones, permitiendo colocar el objetivo de US$ 150 millones a una tasa de 5.89%, confirmando el apetito del mercado. Hay mucha liquidez en dólares en la plaza local y demanda por activos en esa moneda, algo que empresas y provincias vienen aprovechando. Que el Tesoro siga ese camino es una buena estrategia: la operación debería ayudar a comprimir la curva en dólares y dar certidumbre sobre los pagos, contribuyendo a perforar los 500 puntos de riesgo país.

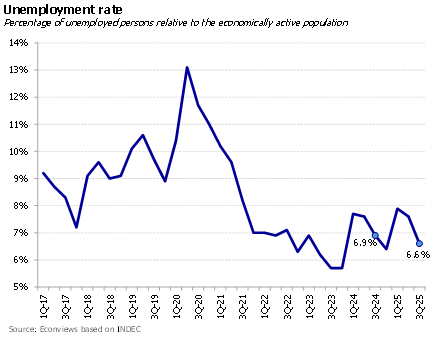

The closure of the Fate tire plant and the debate over labor reform have placed growing concerns about jobs and wages at the center of the stage. The latest survey from the University of San Andrés confirms this shift: according to public opinion, low wages are now the main problem affecting the country, followed closely by corruption and unemployment. Inflation only appears in tenth place—a drastic change from November 2023, when price hikes led the rankings by a wide margin.

The week in the Argentine economy left a bittersweet taste. On one hand, the good news was that the Senate passed the labor reform bill and the Central Bank (BCRA) continued to buy dollars at a steady pace. However, at the same time, inflation served as a reminder that the game was far from over and the opponent was tough to beat, compounded by employment data that were far from encouraging.

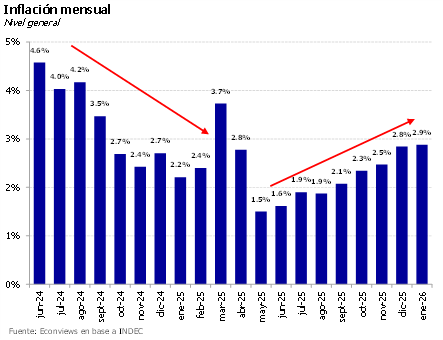

La inflación está difícil de domar. El 2.9% de enero sorprendió negativamente, ubicándose por encima de lo esperado por el mercado y marcando el octavo mes consecutivo de aceleración mensual. La nota positiva es que la inflación núcleo se desaceleró del 3% al 2.6%, y en febrero los aumentos en alimentos vienen siendo más moderados. Con el nuevo índice, la medición habría rondado el 2.7%. Sin embargo, la postergación de la nueva canasta (que otorga mayor peso a los servicios) parece responder más a los ajustes tarifarios pendientes para el resto del año que al dato puntual de enero. Como señalamos habitualmente, la desinflación es un proceso largo y no lineal, pero preocupa la ausencia de un ancla clara. El último REM ya mostraba un repunte en las expectativas. Prevemos que la inercia seguirá pesando y que la inflación cerrará 2026 cerca del 27%.

January closed with a highly positive balance for the Argentine economy. After moving past the electoral noise and with a macroeconomy showing signs of stabilization, the Government managed to make significant progress in reserve accumulation, brought country risk down to the 500-point range, and kept the exchange rate under control. However, February has begun with a slightly more complex scenario, as clouds gather on both the external and domestic fronts.

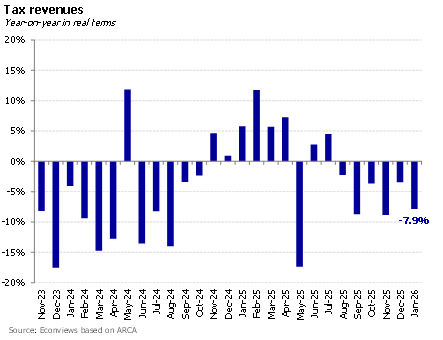

Inflación, INDEC y polémica. Después de un enero tranquilo, el gobierno se autoinfligió ruido innecesario con la decisión de postergar la implementación del nuevo índice de inflación, causando la renuncia del titular del INDEC. No son buenas señales. En un país con una historia de manipulación de estadísticas todavía fresca, la credibilidad cuesta mucho construirla y muy poco dañarla. La decisión también es difícil de entender: si bien en 2024 la diferencia entre ambos índices fue de 16.5 p.p., en 2025 fue de apenas 1 p.p. Con tarifas bastante más alineadas, estimamos que la diferencia tampoco iba a ser significativa en 2026. Yendo al corto plazo, enero pinta para cerrar con una inflación cercana al 2.5%. Nuestro relevamiento de alimentos y bebidas se mantuvo en el 2.8% mensual, y los regulados aumentaron nuevamente cerca de 3.4%. La buena noticia es que registramos una desaceleración importante en alimentos para la última semana del mes.

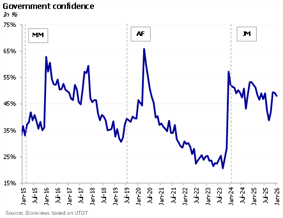

A turning point? After a year characterized by high economic volatility and political uncertainty, the government has strengthened its political position, supported by greater representation in Congress and continued popular backing. Confidence in the administration has recovered to high levels after suffering a significant decline prior to the October elections. This political consolidation has improved governance conditions and enhanced the government’s capacity to advance its policy agenda.

Country risk reached its lowest level since June 2018 last week. The reserve accumulation program was the final push the indicator needed to seek new lows. The market saw results and rewarded them: the Central Bank added USD 1,100 million in January, and the index broke below the 500-basis-point mark.

Suben reservas, baja el riesgo país. El BCRA mantiene la racha compradora con un saldo positivo de US$ 1,083 millones en enero. Esta consolidación del programa de reservas se sumó a un clima internacional favorable: la exitosa colocación de Ecuador (que salió al mercado con 450 puntos de riesgo país) validó el apetito por emergentes y envió una señal positiva para un eventual regreso de Argentina al crédito internacional. El riesgo país perforó los 500 puntos, alcanzando mínimos no vistos desde 2018. Con Ecuador operando en la zona de 413 y la canasta de comparables en 317 puntos, esperamos que el spread argentino siga comprimiendo si el Central sostiene el ritmo de compras.

Since the Milei administration took office, a fierce debate has opened up regarding the future of industry and employment. On one side are those arguing that the economic program is causing an “industricide” and higher unemployment, pressing for the economy to remain protected. On the other side are the free-market fundamentalists who lean towards the idea of leveraging comparative advantages.

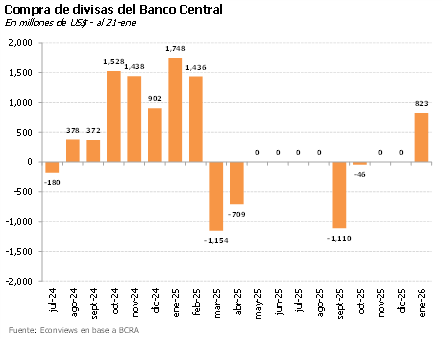

Comprando tranquilo. El Banco Central logra sumar reservas mientras el tipo de cambio se mantiene a raya. En lo que va de enero ya acumuló US$ 822 millones, en un mercado que finalmente aflojó la presión alcista. El bajo volumen operado sugiere que gran parte de las compras se habrían realizado en bloque por fuera del MULC. Juegan a favor las colocaciones de deuda privada, una mejora en la liquidación del agro y una menor demanda de cobertura, disciplinada a fuerza de tasas altas. Por ahora, el riesgo país no logra consolidar la baja, castigado principalmente por el mal humor externo.

Feo dato de inflación. El 2.8% de diciembre estuvo por encima de lo esperado y encendió alguna luz amarilla. Si bien sabemos que el proceso de desinflación no es lineal, y que la inercia juega un papel más fuerte cuando la inflación no es tan alta, la realidad es que los precios se aceleraron por séptimo mes consecutivo. Desde el paso al esquema de bandas, el tipo de cambio dejó de funcionar como ancla nominal, y la política monetaria no ha sido lo suficientemente robusta para coordinar expectativas. Esa falta de un ancla clara es, hoy, lo que más ruido hace de cara al futuro. De todos modos, esperamos mejores números para los próximos meses y una inflación cercana a 25% para todo 2026.

When it was announced in December that the Central Bank would begin accumulating reserves in 2026, many of us were skeptical. The government had consistently missed this explicit target within the IMF program throughout last year and had operated on the edge regarding the external front—to the point of needing a “Trump bailout” to avoid a collapse on the road to the elections.

A new year begins with many challenges but also with hope. Fortunately, it starts with an approved Budget Law and a good chance of moving forward with labor reform. Also, as expected, debt payments were made, providing some peace of mind. However, the challenges remain significant: taming an inflexible inflation rate, ensuring the recovery reaches more sectors and boosts consumption, dropping the country risk by another 100 points to return to the markets at reasonable rates, increasing reserves, and finally lifting capital controls.

Señales mixtas: el BCRA compra y el Tesoro vende. El 2026 arrancó movido. El BCRA puso en marcha el programa de acumulación de reservas y compró más de US$ 110 millones entre lunes y miércoles, una noticia claramente positiva. Sin embargo, el nuevo esquema de ajuste de la banda cambiaria debutó con cierta presión sobre el tipo de cambio. Al Gobierno se lo vio algo nervioso por el precio del dólar y salió a marcar la cancha con ventas del Tesoro, venta de futuros del BCRA y de bonos dollar-linked. Esta mezcla de señales genera dudas: ¿alcanza este tipo de cambio para cumplir la meta de los US$ 10,000 millones que quiere el Central? Veremos.

Recalibramiento del programa. Punto a favor para los econochantas: el Gobierno puso primera y anunció los tan demandados cambios en el esquema de bandas y en la estrategia de acumulación de reservas. A partir de enero, las bandas se ajustarán por inflación pasada. Esto evitará, al menos, que el techo continúe apreciándose en términos reales mes a mes. Si bien es un avance respecto al esquema previo, en la práctica el “piso” se ha vuelto testimonial. Hubiese sido preferible un diseño de bandas de flotación genuinas en lugar de un esquema de “techo cambiario”. Queda por verse si a este nivel de tipo de cambio el BCRA podrá comprar suficientes dólares. Aun así, lo valoramos como un cambio positivo.

The government has decided to shift the focus of its program. The exchange-rate band, which until now had been adjusting at a monthly pace of 1%, will now move in line with past inflation, closer to 2%. More importantly, it announced an explicit plan to accumulate reserves, with monthly purchases of around USD 800–1,000 million. A pragmatic turn that the market had been loudly calling for.

The October elections marked a turning point .

In 2025, the government consolidated its power after achieving a convincing victory in the midterm elections. LLA, President Milei’s party, now holds the largest minority in the lower house, while the Peronists lost their majority in the Senate for the first time since the return of democracy in 1983. This places LLA in a strong position. Although it does not command a majority in either chamber, it can negotiate with provincial parties and the more “reasonable” opposition—including Macri’s PRO—to pass the budget and advance structural reforms. The government does not have a blank check, but it does have enough political leverage to negotiate effectively with Congress.

November’s inflation print came in broadly in line with expectations, but it still raised a yellow flag. It is not alarming for now, although the trend over the past six months has clearly been upward. Core inflation, which better captures underlying dynamics, rose to 2.6%, its highest level since April, and year-on-year inflation accelerated for the first time during the Milei administration.